2026/03/31 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

The Central Bank of Colombia (BanRep) delivered a second consecutive 100bp rate hike to 11.25%, in line with market consensus and expectations. The decision came amid unprecedented institutional tensions, as the Minister of Finance withdrew from the monetary policy meeting before its conclusion and later publicly challenged the central bank’s stance.

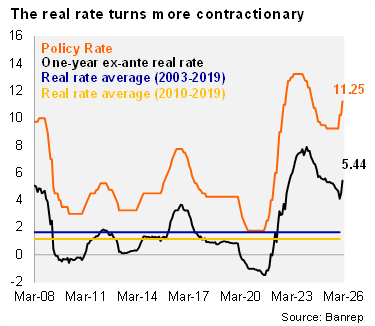

The decision was split: four board members supported the 100bp hike, one voted to keep rates unchanged, and two backed a 50bp cut (including the Finance Minister). Following the rate hike, the one‑year ex‑ante real interest rate climbed to 5.4%, up from 4.1% after January’s meeting and well above BanRep’s estimated neutral real rate of 3.1% for 2026, underscoring the restrictive policy setting.

Inflation remains stubborn. Headline CPI stood at 5.3% YoY in February, above last year’s level, while core inflation excluding food and regulated prices also remains elevated. Although inflation expectations have edged down marginally, market-implied breakevens exceed survey expectations, far above the target. On activity, growth reached 2.6% in 2025, undershooting the technical staff’s 2.9% forecast. External conditions are mixed: geopolitical tensions involving Iran improve terms of trade but raise gas and fertilizer prices, adding new upside risks to inflation. Going forward a data dependent approach is pertinent.

Institutional tensions dominated market attention. In a separate unscheduled press conference, Finance Minister Germán Ávila openly rejected the Board’s decision and called for a broader debate on BanRep’s monetary policy framework, including the use of analyst surveys in rate‑setting. He argued that inflation pressures are largely supply‑driven and external, particularly linked to oil prices, and therefore not responsive to further domestic tightening. In his view, additional hikes risk becoming unnecessarily contractionary, constraining growth while failing to tackle inflation’s root causes. Ávila signaled his intention to step back from future monetary policy meetings, escalating governance risks. In our interpretation of BanRep's governance rules, a minimum quorum of five members—including the Finance Minister—is required to set the policy rate. Also, the decree 2520 of 1993 states that, following two unjustified board member absences, the President must appoint a new member to attend the Board. This raises operational uncertainty ahead of the next decision meetings on April 30 and June 30. Should quorum issues arise, the authorities may need to rely on alternative tools, such as adjustments to reserve requirements, to maintain policy traction.

Villar underscored that the Board’s decisions are aimed at fulfilling its constitutional mandate. Following the MoF’s remarks, Governor Villar emphasized that all Board members act based on what they believe is best for society as a whole, in line with the constitutional mandate to preserve the purchasing power of the Colombian currency. Finally, Villar noted that if the MoF were to decide not to attend future Board meetings, it would constitute a breach of a constitutional mandate.

Our take: Inflation risks remain clearly skewed to the upside, reflecting persistent indexation, uncertainty around the minimum wage hike, high global oil prices, and rising El Niño risks in 2H26 through food prices. Despite softening growth, inflation expectations remain unanchored, reinforcing the case for a restrictive stance. While institutional frictions complicate the outlook, we continue to expect further tightening at the April 30 meeting, contingent on quorum. Markets are likely to increasingly price credibility and governance risks alongside traditional inflation‑growth dynamics to macroeconomic variables.