2026/04/29 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

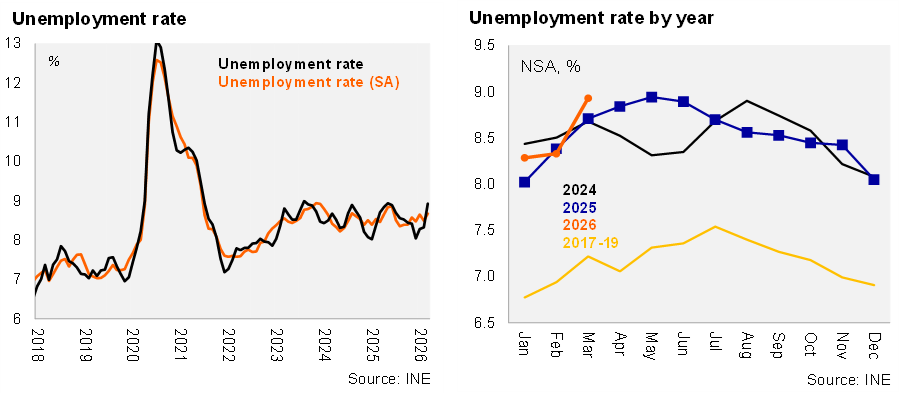

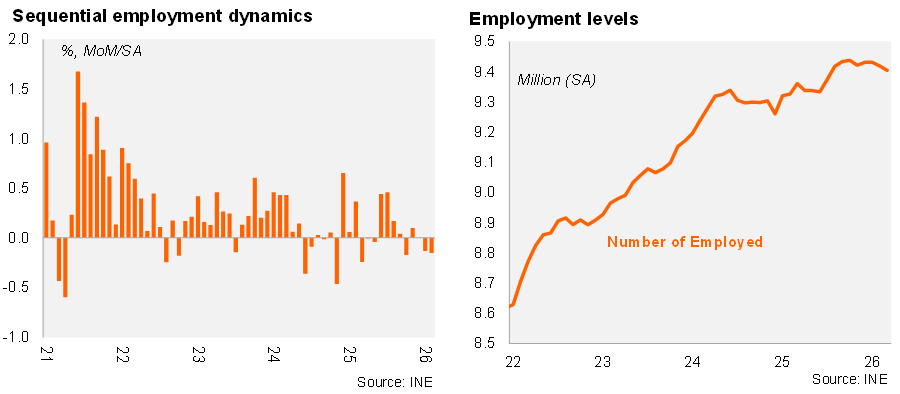

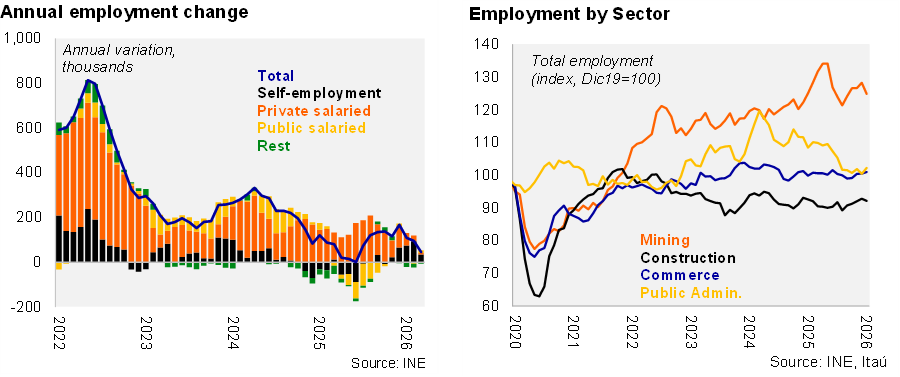

According to the National Statistics Institute (INE), the unemployment rate during the first quarter of the year was 8.9%, well above market estimates (Bloomberg consensus and Itaú: 8.6%). The unemployment rate sits 0.2pp above what was recorded in 1Q25 and is the highest 1Q rate since 2021. Adjusting for seasonal factors, the unemployment rate rose by 0.2pp from 4Q25. Labor force participation reached 62.3%, down 0.1pp year-on-year. Total employment increased by 0.5% over the past twelve months (around +45 thousand jobs), slowing from the 1.8% in 4Q25, largely driven by a 3.2% annual rise in informal employment, while formal jobs declined by 0.5%. The informality rate rose 0.7pp over the last year to 26.5%. By sector, health services (6%) and professional activities (8.8%) made the strongest positive contributions to annual employment growth, whereas public administration continued to be the main drag. Total hours worked dropped 0.1% year-on-year and average hours declined 0.5% to 35.7 hours, in line with the implementation of the 40-hour work week reform. The expanded unemployment measure (including potential labor force) rose to 17.4% (+0.5pp), pointing to significant underutilized labor with women disproportionately affected.

Our Take: The data continue to point to a labor market with significant slack, still absorbing the unprecedented increases in labor costs seen in recent years, and consistent with activity indicators that have come in weaker than expected. In fact, some indicators of labor demand remain quite depressed, while measures of job destruction — such as unemployment insurance beneficiaries — increased 8.6% year‑on‑year in February. In this context, public policies that help mitigate further increases in labor costs would support a gradual recovery in Chile’s labor market. This reinforces the importance of swiftly advancing policies such as the tax credit aimed at encouraging formal employment. Labor market slack, together with the erosion of real incomes due to higher expected inflation, is constraining private consumption growth this year. Reviving private investment is essential. We expect GDP grwth of 2.1% this year (2.5% in 2025), with the boas tilted to the downside.