2026/02/27 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

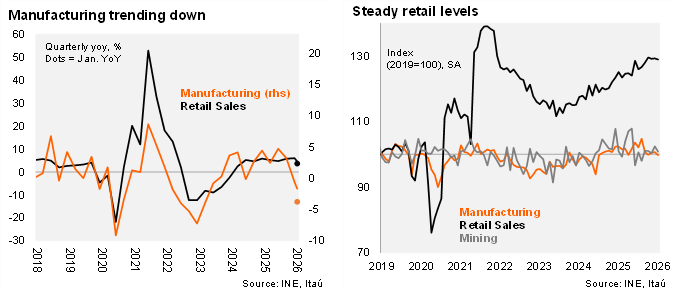

According to the INE, real retail sales rose by 3.7%, slightly below Bloomberg’s median (4.0%) but closer to our call (3.6%). The product categories that contributed most to annual growth were food (1.1pp), clothing, footwear and accessories (0.77 pp), and miscellaneous consumer goods (0.73 pp), with increases of 4.7%, 5.6%, and 5.0%, respectively. Sequentially, real retail sales fell 0.2% MoM SA in January, reversing the +0.1% increase observed in December. Meanwhile, manufacturing production fell by 3.8% YoY, significantly weaker than both the Bloomberg median (-1.5%) and our call (-0.8%). This decline was mainly explained by a 15.9% annual drop in machinery and equipment manufacturing (contributing -0.74 pp) and an 8.5% decrease in chemical products manufacturing (-0.66 pp). These results reflect a slowdown in project development within the mining sector and production stoppages in companies within the chemical segment. Sequentially, manufacturing contracted 0.9% MoM SA, breaking a two-month streak of sequential increases. Mining output decreased 0.1% YoY, with a seasonally adjusted monthly contraction of 1.6% (following +2.1% in December). The INE reported mining stoppages during the month, an issue to monitor going forward given the historically significant impact of mining-related shocks. Also, several wage negotiations are scheduled in the mining sector this year. Overall industrial production fell 1.6% YoY, below the market median (-0.4%). Taken together, these results suggest that January’s Imacec would rise by 1% YoY, slowing from December (1.7%), and marking the slowest increase since August (0.3%). Weak sectoral activity takes place in the context of a broader soft patch seen in overall macro data in Chile, evident in January's credit and labor market data.

January data suggests that marginal momentum is softening. Retail sales posted a 3.4% QoQ/SAAR increase in the quarter ending in January, down from the 8.1% recorded in 4Q25. Meanwhile, manufacturing production contracted 5.7% QoQ/SAAR (following -8.3% in 4Q25), extending its sequential weakness. Mining output grew 4.7% QoQ/SAAR (+5.6% in 4Q25), resulting in overall industrial production showing a slight contraction of 0.1% (-1.1% in 4Q25).

Our take: Weaker than expected sectoral data in January takes place in a broader patch of soft data, contrasting with the persistent upside revisions to growth forecasts. Looking ahead, the January IMACEC, to be released on Monday, March 2, and the national accounts data revising last year’s GDP figures, to be published on March 18, will be key for assessing the current momentum of activity at the margin and for evaluating the likelihood of achieving growth above potential this year. Achieving our projected 2.6% GDP growth for this year implies a significant sequential acceleration in the coming quarters.