2026/06/30 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

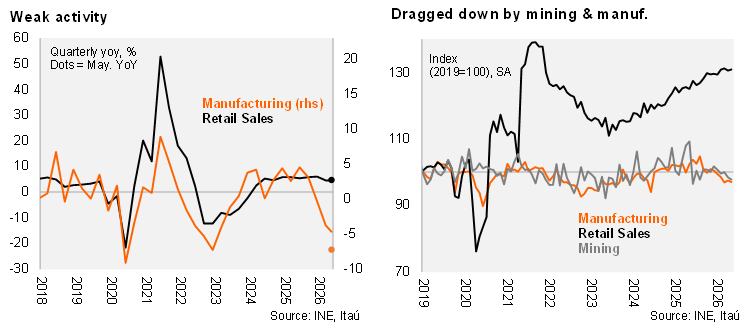

According to the INE, real retail sales rose by 4.8% YoY, somewhat below market expectations of 5.5% but closer to our call (5.0%). The main contributors to the increase were clothing, food, and household equipment—particularly electronics—with annual gains of 8.9%, 4.0%, and 6.9%, respectively. On a seasonally adjusted basis, retail sales rose 0.3% MoM, partially reversing the 0.5% decline recorded in April. In contrast, manufacturing output collapsed by 7.2% YoY, significantly below market expectations of a 2.7% decline and our call of -2.5%. The weakness was largely explained by lower fish production, reflecting adverse weather conditions that reduced biomass availability in usual fishing areas. In monthly seasonally adjusted terms, manufacturing fell 0.5%. Mining output also nosedived, falling by 10.6% YoY, driven by a high comparison base and lower ore grades at major companies in the sector. On a monthly seasonally adjusted basis, mining decreased 0.7%. Overall, industrial production dropped 7.5% YoY—well below market expectations of a 4.5% increase—and declined 0.4% month-over-month on a seasonally adjusted basis.

Activity at the margin doesn’t pick up. For the quarter ending in May, industrial production contracted 5.2% YoY (vs. -3.2% in April), while real retail sales grew 4.5% YoY (broadly in line with 4.7% in April). On a sequential basis, industrial production contracted 7.3% QoQ/SAAR (vs. –7.4% in April), with manufacturing decreasing 9.2% and mining shrinking 7.4% QoQ/SAAR (vs. -10.2% and -5.9% in April respectively). Real retail registered 3% QoQ/SAAR, losing momentum from April (+4.4%) but still in positive ground.

Our take: Taken together, the data points to ongoing weakness in activity at the margin spilling through to 2Q26. Retail sales are likely to remain subdued in the context of lower foreign tourism inflows and the decline in household confidence. Importantly, the El Niño phenomenon is likely taking a (transitory) toll on specific sectors, such as fishing. Activity data has yet to show signs of a cyclical improvement as we enter the second semester, as hinted by ongoing annual real contractions in bank credit data. Our forecast for the May IMACEC, to be published by the BCCh tomorrow, is -0.6% YoY for headline and +1% YoY for non-mining IMACEC.