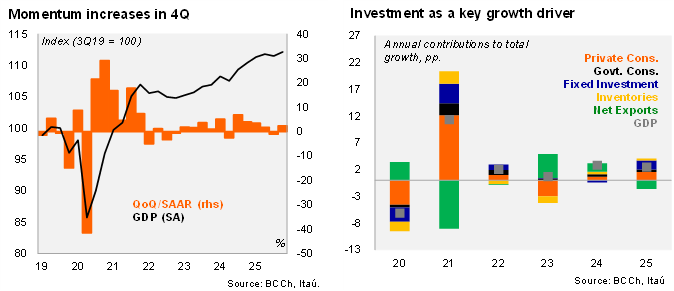

According to the BCCh, real GDP rose by 2.5% in 2025 — two tenths above the preliminary monthly GDP estimate. From the expenditure side, investment rose by 7% in 2025, after 2024 contraction of 1.6% and marking the strongest growth since 2021 (+16%). Private consumption increased by 2.7% (vs. 1.1% in 2024), with all its components contributing positively to overall growth. The largest boost came from spending on nondurable goods, particularly clothing and food purchases. Meanwhile, government consumption increased 3% (up from 2.8% in 2024). Total exports rose 4.6%, while imports surged 10.5%, resulting in a negative net contribution to economic activity. The increase in goods exports was consistent with higher fruit shipments—especially cherries—whereas growth in goods imports reflected greater purchases of machinery and equipment, particularly electrical and electronic devices, as well as transportation vehicles. Our February Imacec nowcasts sits at 1.3% YoY.

At the margin, economic activity increased its momentum. GDP rose by 0.6% QoQ/SA in the 4Q25, reversing the -0.3% contraction of the third quarter. Non‑mining GDP also grew 0.6% in 4Q25 (+0.5% in 3Q). On the expenditure side, private consumption increased 0.9%, with all components contributing positively, while government consumption fell -1.5%. Investment rose 1.0% in 4Q25, maintaining strong momentum throughout the year, although moderating at the margin (with sequential quarterly growth of 1.9%, 2.7%, and 3.8% in 1Q, 2Q, and 3Q, respectively). Finally, GDP grew 2.3% QoQ SAAR in 4Q, after declining -1.1% in 3Q.

Following the BCCh’s regular National Accounts revisions, GDP growth was revised upward for 2023 and 2024 (from 0.5% to 0.7% and from 2.6% to 2.8%, respectively).

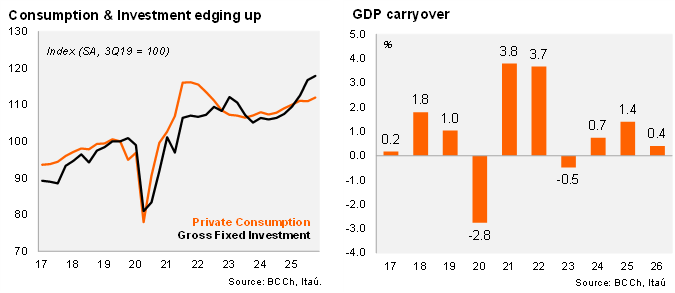

Our view: Looking through the rearview mirror, the national accounts data confirms the economy is experiencing an investment-led recovery, albeit with a softer start to 2026. In fact, the statistical carry-over for 2026 is a mere 0.4%, below 2025 (1.4%) and 2024 (0.7%). In addition, the monthly GDP proxy for January was sharply revised down, from -0.1% to -0.5% (MoM/SA was revised down from 0% to -0.2%), prior to the conflict in the Middle East. Our 2026 GDP forecast of 2.6% considered an important sequential acceleration of economic activity in the coming quarters. Tighter global financial conditions and higher oil prices are likely to weigh on economic activity.