2026/03/31 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

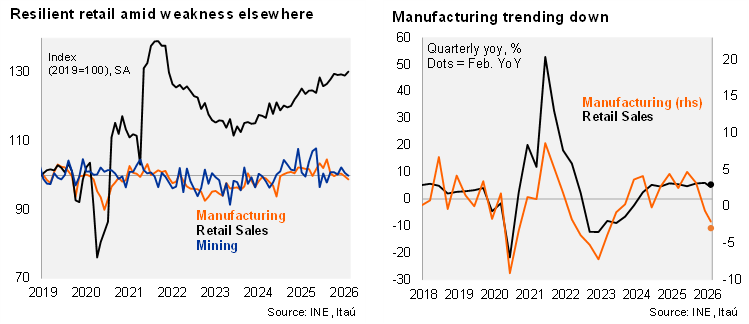

According to the National Statistics Institute (INE), retail sales rose 5.4% YoY in February (January: 3.6%), beating both the Bloomberg consensus (4.4%) and our 5.0% forecast. Growth was driven by electronics (+10.7% YoY) and apparel (+6.6%). On a month‑over‑month basis, retail sales increased 0.9% (SA), reversing the mild contraction seen at the start of the year. In contrast, manufacturing output contracted 3.0% YoY (January: ‑3.6%), substantially weaker than consensus expectations (‑0.4%) and our call (+0.5%). The decline was largely explained by fish‑meal production, which subtracted 3.2pp, reflecting unfavorable base effects after last year’s early fishing season. On a sequential basis, manufacturing fell 0.9% m/m (SA). Mining activity showed marginal improvement, growing 0.2% YoY, the first expansion since May 2025, but still declined 0.8% m/m (SA). As a result, overall industrial production contracted 1.3% YoY, broadly in line with January’s outcome.

Momentum cooling across sectors. Retail sales rose 1.9% QoQ/SAAR in the quarter ending February, down sharply from 8.3% in 4Q25, marking the weakest pace since 3Q24. Meanwhile, manufacturing output fell 2.3% QoQ/SAAR, extending its contractionary trend, while mining posted a modest 1.2% QoQ/SAAR increase.

Our Take: We expect the February IMACEC to increase by 1.0% YoY (January: ‑0.5%), supported by consumption. Credit dynamics remain weak, with total bank loan growth holding at 2.2% YoY (nominal), unchanged from January, pointing to subdued demand. The labor market remains soft, with stagnant employment and slowing wage growth reinforcing downside risks. Looking ahead, the rapid pass‑through of higher energy prices and elevated geopolitical uncertainty are likely to weigh on both business and consumer confidence, limiting near‑term activity momentum. We see 2026 GDP growth at 2.1% (from 2.5% in 2025). While near‑term growth risks are tilted lower, the investment pipeline continues to progress, preserving a constructive medium‑term outlook. From a monetary policy perspective, higher short‑term inflation (4.1% by year‑end) alongside softening activity leaves the central bank facing competing signals. We expect the Board to remain data‑dependent, maintaining a meeting‑by‑meeting approach, with a bias toward holding the policy rate at 4.5%, unless medium‑term inflation expectations become unanchored. The minutes of the March MP meeting will be released on Wednesday.