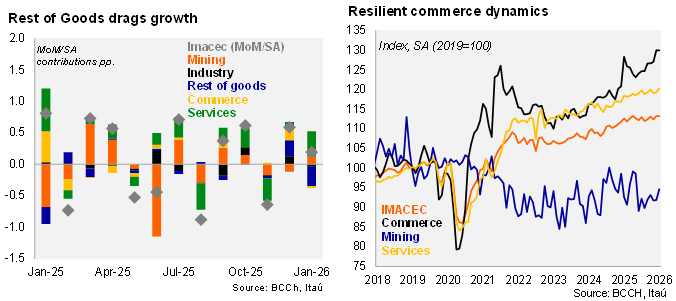

According to the Central Bank, January’s monthly GDP proxy (Imacec) contracted by 0.1% year‑on‑year during the first month of 2026 (1.7% in December), well below the Bloomberg median and our call of +1.0% (EEE: +1.9%). This is the first annual contraction since June 2024. The annual decline was led by mining, manufacturing, and agriculture. Services grew by 1.4% YoY, while non-mining activity was flat on an annual basis. The bulk of the surprise to our call stemmed from agriculture. Cherry exports (peaking in December and January), posted a 20% nominal decline at the start of the year. On a sequential basis, the seasonally adjusted series increased by 0.2% MoM/SA, pulled up by the 0.8% services gain, while rest of goods (agriculture) fell 2.3%. Holding activity at the levels of the latest rolling-quarter (SA) for the remainder of 2026 would lead to carryover growth of 0.3%. Our preliminary estimate for February IMACEC is 1.8%, aided by more favorable base effects.

Activity dynamics show commerce is holding up well, while services momentum slows. Sequentially, the economy grew at an annualized rate of 1.4% (QoQ/SAAR), pulled up by a near 9.9% gain in commerce. Services grew a mild 0.8% QoQ/SAAR, while mining contracted 0.7%.

Market sentiment remains upbeat, but credit dynamics have yet to respond. Business sentiment in February consolidated its favorable stance at the start of the year (52.3; 50 = neutral), the highest level over the last four years. Excluding mining, business sentiment neared neutral levels (not seen since early 2022). While consumer sentiment in February remains a tick below neutral levels at 45.1 points, the one-year country outlook continues to pull the index up. Despite improving investment performance, lower interest rates, inflation and sentiment, bank credit has yet to turn the corner. The stock of outstanding bank credit in the Chilean system rose nominally by only 1.9% YoY during January (2.8% inflation).

Our Take: The weak end to last year and soft start to 2026 requires the economy to swiftly recoup momentum to meet our 2.6% growth call (2.3% in 2025). The BCCh will release national accounts data on March 18, often bringing relevant historical data revisions. Overall, even though activity has recently been in a soft patch, we believe the favorable terms‑of‑trade shock, combined with lower interest rates and declining inflation should consolidate the economic recovery. We assume the mining sector will return to growth this year, while elevated copper prices continue to support investment dynamics and related services. How does the BCCh react? With activity having been weaker-than-expected in recent months and inflation passing below the 3% target, the market will question whether the BCCh should extend the cutting cycle beyond 4.25% (rate cut expected later this month). We believe the recovery in business and consumer sentiment and continued upward revisions to the private investment pipeline amid a scenario of lower interest rates and inflation will lead the BCCh to expect a domestic demand recovery ahead that will diminish downside inflation pressure and avoid the need to take the monetary policy rate towards expansionary territory. Monitoring the evolution of medium-term inflation expectations will also be key in anticipating the BCCh’s next move. The two-year inflation outlook has remained anchored to the 3% target, while the latest shock to oil prices and CLP will likely prevent CPI expectations from consolidating below the target.