2026/03/24 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

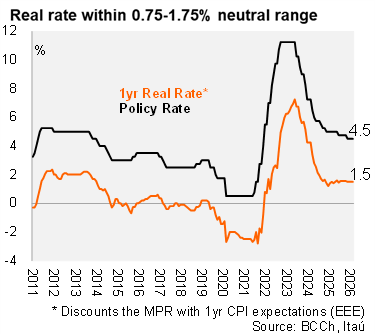

As expected, the Board of the Central Bank unanimously voted to keep the policy rate at 4.5% and withdraw prior signaling of further easing. The forward guidance is now neutral with policy firmly in wait-and-see mode. The Board acknowledged a sharp deterioration in the global environment following the escalation of the Middle East conflict, with elevated oil prices, tighter global financial conditions, and a renewed risk‑off tone weighing on asset prices and currencies, including the CLP. The press release suggests that the BCCh sees no immediate need to react to a supply‑driven inflation shock but is vigilant given the magnitude and speed of the oil price increase. Focus will be on pass-through dynamics and broader persistence of the shock. Clearly, risks tilt towards the next rate move being a hike rather than a cut. Using the BCCh’s analyst survey, the ex-ante one-year real rate remained at 1.5pp, within the neutral range (0.75% to 1.75%), however if one-year breakeven inflation is utilized, the ex-ante real rate drops to near zero (1.5pp at the January meeting).

Prior to the oil shock, inflation dynamics had continued to improve at the margin. Headline CPI stood at 2.4% YoY in February, while core inflation remained near the target. However, the BCCh now expects headline inflation to climb to around 4% YoY in 2Q. Consistent with the view of a transitory shock, the Board highlights that the key two‑year inflation expectations remain anchored near 3%.

Recent activity data came in softer than expected, partly reflecting supply disruptions in mining and agriculture. On the demand side, private consumption remains resilient and investment continues to be supported by mining and energy projects, while recent fiscal announcements point to tighter spending conditions ahead. Financial conditions have tightened in recent weeks, mirroring global trends, with higher rates across the curve and weaker equity markets.

Up next. On Wednesday, the BCCh will release its Monetary Policy Report (IPoM) that will likely raise short-term inflation and reduce the positive output gap that was previously envisioned. The signaled rate path will likely lean towards stability ahead as the Board takes time to gauge the appropriate policy response. The minutes of the meeting will be published on April 1, and the next decision is scheduled for April 28.

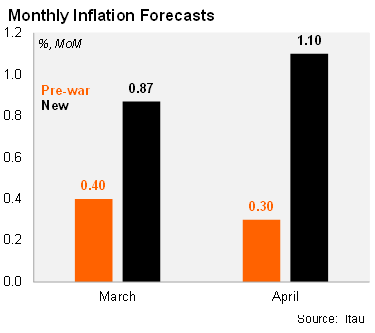

Our Take: The abrupt pass‑through of international oil prices into domestic prices will materially lift short‑term inflation forecasts. Our inflation projection for the March–April period has risen sharply from 0.7pp prior to the Middle East conflict to close to 2pp. As a result, year‑end inflation is now highly likely to exceed 4%, conditional on the evolution of global oil prices. The magnitude of the recent shock also raises the risk of a faster propagation of second‑round inflation effects. In this context, should inflation expectations at the policy‑relevant horizon begin to move persistently above the Central Bank’s target, policy rate hikes would come into play—although this is not part of our baseline scenario. It is also important to note that higher oil prices increase costs for both households and firms, weighing on economic activity over time. Ensuring that the investment recovery remains on track and broadens across sectors will therefore be critical and remains a key assumption underpinning our base case.