2026/03/25 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

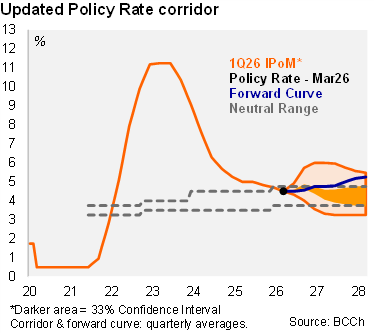

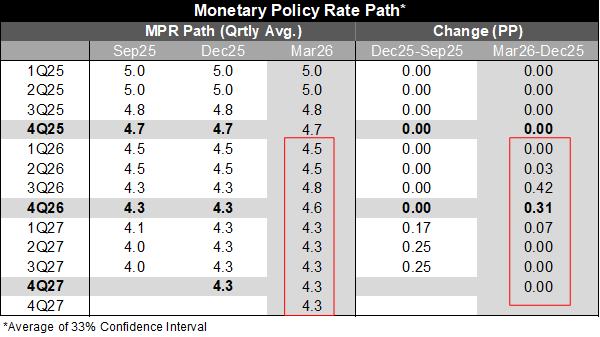

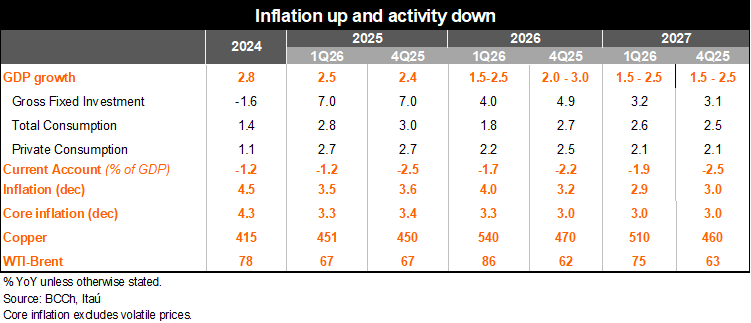

As expected, the BCCh’s economic update marks a turning point in the macro narrative, shifting from a benign normalization story toward one dominated by external shocks and uncertainty. Until early 2026, the economy had evolved broadly as expected with activity growth near potential and inflation converging faster than anticipated, dipping to 2.4% year‑on‑year in February, slightly below the 3% target. However, the outbreak of war in the Middle East materially altered the outlook, triggering a sharp rise in international energy prices and global and domestic uncertainty. With the shock redefining the near‑term macro balance (higher inflation, lower growth), the BCCh was forced to reassess the adequate policy strategy. The updated rate corridor wipes out a prior cut to 4.25% this year, with the balance of the risks tilting towards higher short-term rates. The Middle East conflict is incorporated in the baseline scenario through higher energy prices and tighter global financial conditions. The Brent-Oil average forecast for the year now sits at USD 86 per barrel (previously USD 62).

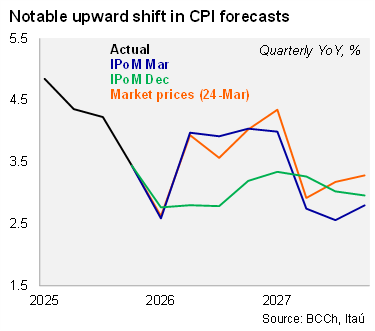

Inflation registered the most drastic change. While the disinflation process up to February proved faster than the BCCh was anticipating, a significant short‑term reacceleration is now penciled in, with headline inflation rising toward 4% from the second quarter of 2026 onward (+0.8pp from the December scenario). This increase is largely attributed to higher fuel prices, with the explicit comment that the Government's fuel price hike was incorporated into the baseline scenario. Of note, the BCCh emphasizes that this is primarily a supply‑driven shock rather than a demand imbalance. Nevertheless, the inflation spike delays convergence to the 3% target, which is now seen occurring in early 2027 rather than early this year as previously expected.

Against this inflation backdrop, the growth outlook was downgraded. The 2026 GDP growth forecast range shifts to 1.5%–2.5%, down 0.5pp from the December scenario. This downgrade reflects a combination of a less supportive global environment, weaker mining output, and the fiscal consolidation announced in mid‑March, amounting to roughly USD 3.8 billion. The tightening of fiscal policy weighs on public consumption and investment, while private consumption and investment expectations were also revised slightly lower due to worsening external conditions. These drags are only partially offset by continued real wage growth, improved expectations, and a relatively strong pipeline of investment projects compared to previous years. As a result, the output gap is seen as somewhat negative over the forecast horizon (versus the more upbeat view in December). An economy operating near potential, with interest rates close to neutral supports the view that once the supply shock dissipates inflation will swiftly reconverge to the target. The 10-year trend GDP estimate was revised up by 0.1pp to 1.9%.

The monetary policy strategy, amid heightened uncertainty, shifts to a meeting-by-meeting approach. The Board unanimously kept the policy rate at 4.5% this month. The Board highlights the need to continuously reassess alternative scenarios, particularly those in which global shocks could generate more persistent inflationary pressures. Future decisions are likely to be more reactive to the global context and its impact to local conditions, a shift from the predictable normalization path undertaken to date. As a result, the midpoint of the updated corridor signals a 25bps hike during 3Q26, where the upper bound of the rate corridor outlines that the policy rate could reach 6% during 2H26 if inflation turn out to be higher and more persistent than currently projected.