2026/06/16 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

The decision. As widely expected, the BCCh’s Board unanimously kept the policy rate on hold at 4.5%. Forward guidance was essentially unchanged, where despite the recognition that inflation risks have been more balanced, the Board maintained a data-dependent, meeting-by-meeting approach amid persistent uncertainty.

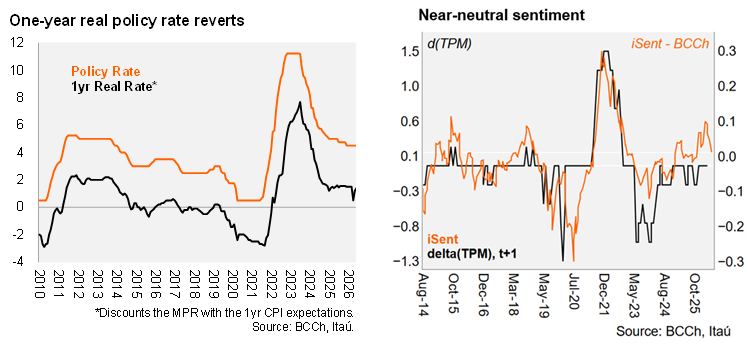

The 1yr ex-ante real rate moves back into neutral range. With inflation expectations converging back to target, the one-year ex-ante real policy rate rose to 1.4% (from 0.5% in April), placing it back within the BCCh’s estimated neutral range (0.75–1.75%).

External backdrop improving at the margin. Developments in the Middle East now point to a potential agreement, with oil prices retreating and global equities rallying. In response, the government reiterated its commitment to accelerate the pass-through of lower international fuel prices, scrapping the usual lag in the smoothing mechanism.

Domestic macro: weak activity, anchored expectations. Inflation has evolved broadly in line with expectations, with medium-term expectations remaining anchored. Activity has been softer than anticipated—primarily reflecting supply-side disruptions—while labor market conditions remain weak. On the fiscal front, the drag appears somewhat less pronounced than expected as of March.

Our take: We expect a prolonged pause at 4.5%. The current stance appropriately balances still-elevated uncertainty with anchored expectations, allowing the Board to closely monitor inflation expectations and pass-through dynamics.

Upside risks: Potential second round effects a drift in policy-relevant inflation expectations above target, or more persistent cost pressures would make rate hikes a tangible option.

Downside risks: A sharper deterioration in the labor market leading to a faster disinflation process could shift market pricing toward eventual easing.

In the near term, we expect the June IPoM to signal weaker short-term growth while preserving the view that inflationary pressures are transitory, resulting in a symmetrically distributed policy rate corridor. While the March IPoM projected 1.5%–2.5% growth for 2026, our updated estimate is at the bottom of the range (1.5%).

Key dates:

- 2Q26 IPoM: June 17

- MPM minutes: June 24

- Traders Survey: July 02

- June CPI: July 08

- Next MPM: July 28