2026/04/28 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

The decision. As expected, the BCCh’s board unanimously maintained the policy rate at 4.5%, in line with our call and the broad consensus. The forward guidance was reiterated, keeping the “meeting-by-meeting” approach consistent with elevated uncertainty and the materialization of the alternative scenarios outlined in the March IPoM.

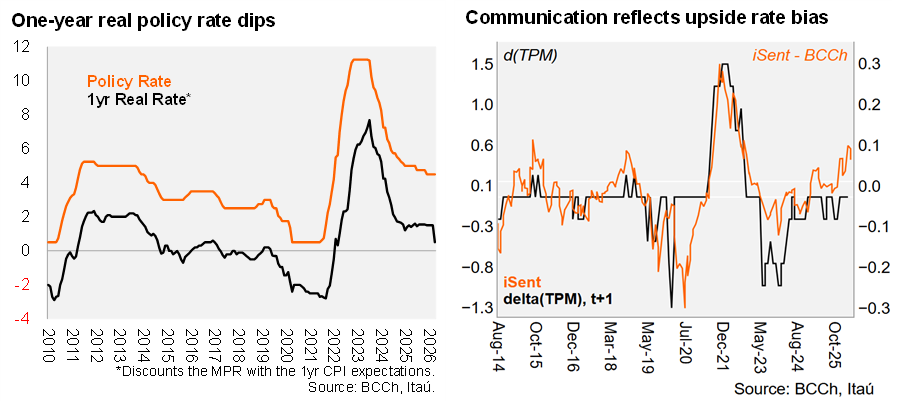

1yr ex-ante real rate swings expansionary. With the one-year ahead analyst median inflation expectation at 4.0%, the one-year ex ante policy rate fell to 0.5%, below the BCCh’s real neutral range (0.75-1.75%).

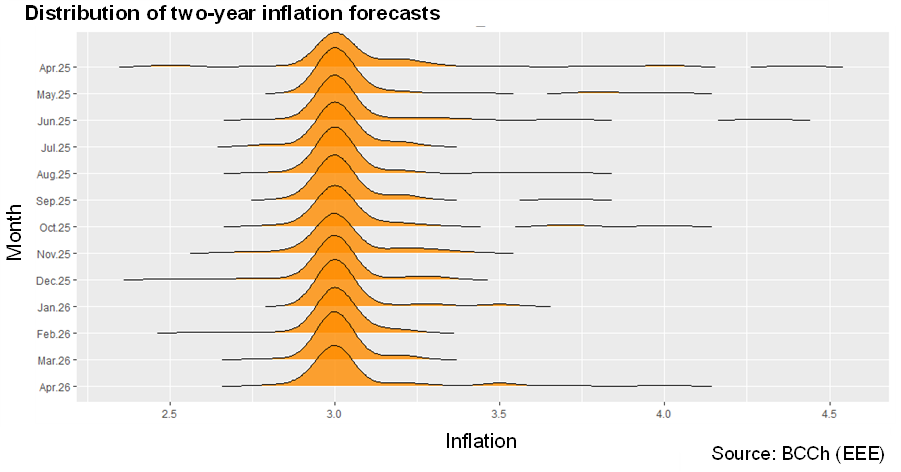

Adverse developments in the Middle East. The statement reveals that developments in the Middle East have been more adverse than in the IPoM’s baseline scenario, raising the probability of negative effects for inflation and global activity. Domestically, short-term inflation forecasts have increased. As such, the BCCh is paying special attention to factors that may lead to greater inflation pass-through and/or persistence.

Our take: BCCh opens the door for hikes, conditional on the inflation outlook. The Board likely discussed maintaining the policy rate in this meeting, along with a 25bp hike. Our forecasts include a significant increase in short-term inflation, mainly reflecting the fast pass-through of international oil prices to domestic ones. However, activity data has been weaker than anticipated, as headwinds stemming from the Middle East conflict are set to weigh further on sentiment and the growth outlook. We see the BCCh on hold at 4.5% for a prolonged period. Should inflation expectations at the policy‑relevant horizon begin to move persistently above the Central Bank’s target, policy rate hikes would come into play.

Keep an eye out for:

- The BCCh’s monthly analyst survey to be released on May 12, shortly after April’s inflation print (May 8), is an important watchpoint.

- The meeting’s minutes will be published on Thursday May 7, and the next monetary policy meeting is scheduled for June 16. The June decision will include two inflation and IMACEC prints.

- If international oil prices decline swiftly, the government has pledged to scrap the smoothing mechanism’s usual lag and adjust domestic prices fast, which will ripple through Chile’s inflation and policy rate forecasts.