2026/04/08 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

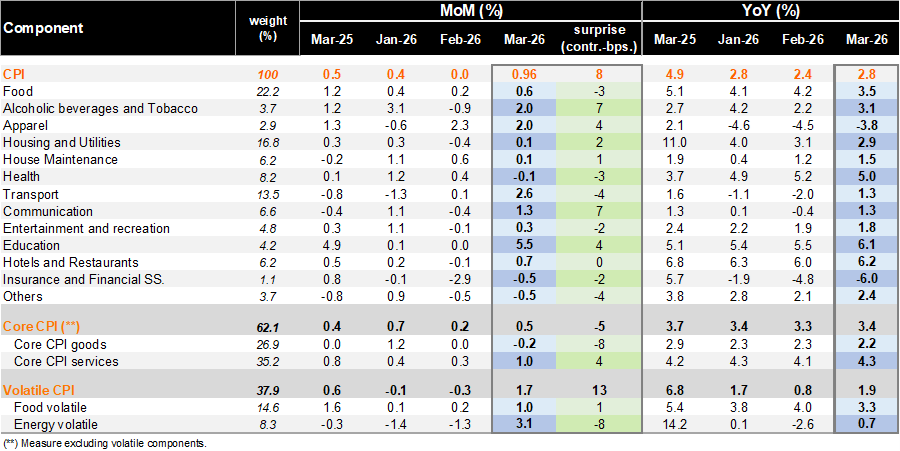

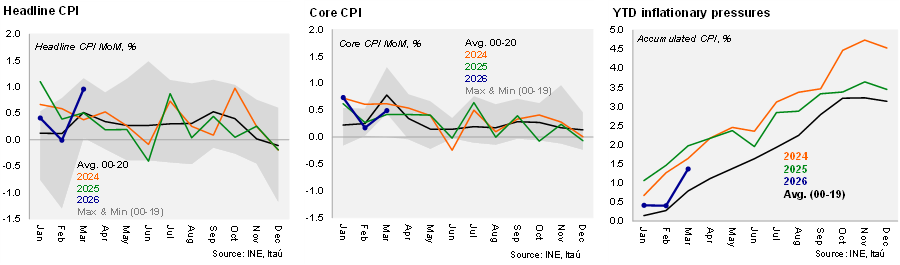

Headline inflation re‑accelerates as energy pass‑through bites. According to the INE, consumer prices rose 1.0% MoM, slightly above both the Bloomberg median and our forecast (0.9%), and the 0.8% implicit in the March IPoM. The monthly increase was driven by energy prices, with gasoline jumping 8.2% MoM (+20bp contribution) after the government unexpectedly accelerated the pass‑through of higher global oil prices to domestic fuel prices. International airfares also surged (+15% MoM; +10bp), while the seasonal education adjustment surprised to the upside (+5.5% MoM; +20bp). As a result, headline inflation rose to 2.8% YoY (from 2.4% in February). Core CPI increased 0.5% MoM, lifting the annual core print to 3.4% YoY (3.3% in February). Goods prices continued to contract sequentially, while services rose 1.0% MoM, driven primarily by education and hotels. Overall, core inflation was broadly in line with expectations (IPoM: 0.44%; Itaú: 0.57%), but near‑term upside risks are clearly building. Looking ahead, we expect inflation pressures to intensify further. Our preliminary April headline CPI forecast is 1.4–1.6% MoM, taking YoY inflation to 4.2%, with core inflation at 0.3–0.4% MoM.

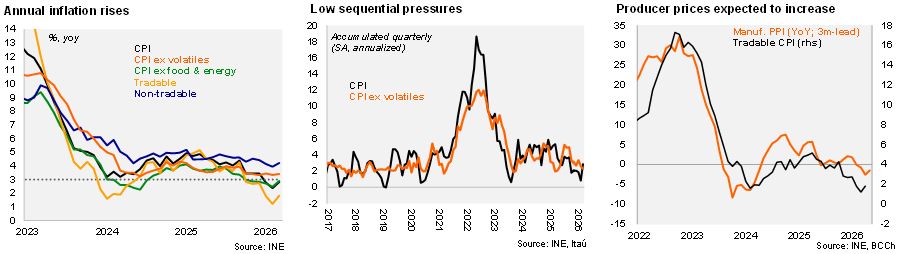

Core pressures remain contained, for now. Sequential core dynamics remain relatively well‑behaved, though momentum is set to pick up. At the margin, annualized inflation accumulated over 1Q26 reached 2.9% (vs. 2.1% in 4Q), while core inflation averaged 2.3% (down slightly from 2.7% in 4Q). Both core goods and services hovered near 2.5% annualized over the quarter. Volatile components rebounded meaningfully in March. Volatile inflation rose to 1.7% YoY (from ‑0.3% in February), with food inflation at 3.3% and energy inflation turning positive at +0.7% YoY (from ‑2.6%). Excluding food and energy, inflation stood at 2.9% YoY. While the magnitude of the energy shock raises the risk of second‑round effects, underlying macro conditions argue against a sustained inflation spiral. Nominal wages grew ~5% YoY in February, well below the 2022–25 average (~8.4%), labor market slack persists, and credit growth remains subdued. Importantly, activity data prior to the Middle East escalation already pointed to an economy lacking momentum, reinforcing the view that inflation pressures remain largely cost‑driven rather than demand‑led.

Our take: Inflation to worsen before it improves, keeping monetary policy on hold unless expectations shift. We continue to see the inflation profile as front‑loaded, with conditions likely to worsen before improving. We hold an upside bias to our 4.1% yearend inflation forecast. In recent remarks, the BCCh governor reinforced a message of caution over commitment, balancing stickier inflation against weakening growth. With price pressures driven by external and cost shocks, the BCCh will prioritize expectations anchoring, reinforcing a firmly data‑dependent policy stance. Notably, the BCCh trader survey (submitted before the March CPI) already reflected this dynamic: one‑year inflation expectations rose to 4.9%, while the two‑year forecast sits at 3.2%. The 1Y1Y forward continues to trade close to target, suggesting medium‑term credibility remains intact. Following recent Middle East developments, market pricing should continue to re‑anchor medium‑term inflation expectations and reduce the probability of rate hikes in 2026 (the curve had been pricing in up to two hikes). From here, managing the narrative around transitory shocks will be critical. The next monetary policy decision is scheduled for April 28, with the BCCh analyst survey due on April 10.