2026/06/30 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

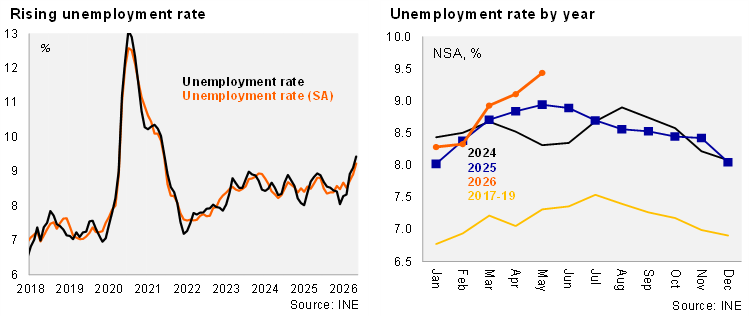

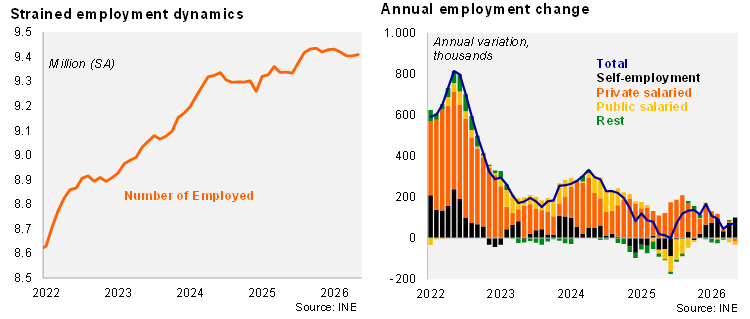

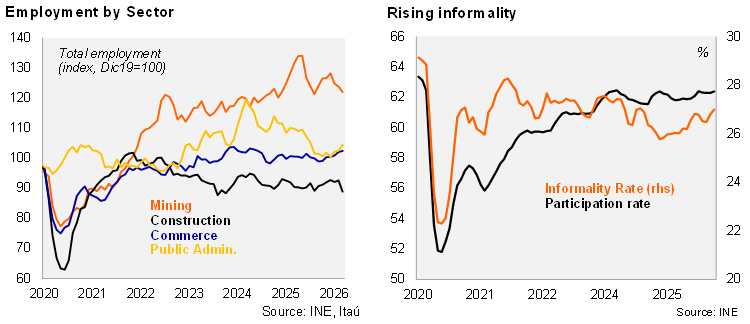

According to the National Statistics Institute (INE), the unemployment rate during the quarter ending in May rose to 9.4%, above market estimates (Bloomberg consensus and Itaú: 9.2%), and the 8.9% registered one year ago. Adjusting for seasonal factors, the unemployment rate edged up to 9.2% (8.7% in 1Q26). Labor force participation reached 62.4%, up 0.2pp year-on-year. Total employment increased by 0.8% over the past twelve months (0.5% in 1Q26), largely driven by a 4.6% annual rise in informal employment. The informality rate rose 1.0pp over the last year to 27%. Overall, the labor force rose by 1.3% (0.7% in 1Q26). By sector, manufacturing (5.2%) and health services (6.0%) posted the most relevant gains. Average hours worked per week declined 0.8% with respect to May-25 to 37.0 hours. The expanded unemployment measure (including potential labor force) reached 17.1% (+0.4pp), pointing to significant underutilized labor with women disproportionately affected (20.3%).

Our Take: The data continues to point to increasing slack in the labor market, as it continues to absorb the unprecedented labor cost increases of previous years, and consistent with weaker than expected activity data. The female unemployment rate reached 10.5%, a level not seen beyond periods of significant shocks. Labor market slack, together with the erosion of real incomes due to higher expected inflation, should constrain private consumption growth dynamics this year. Our forecast for June implies a 9.1% average unemployment rate during 1H26 (8.8% during 1H25). With activity data still weak, and labor market slack growing and the inflation shock falling short of market expectations, the market-implied policy rate path will likely consolidate a partial pricing of lower rates later this year. Our baseline monetary policy scenario remains unchanged, with the policy rate at 4.5% over the forecast horizon as the Board favors accumulated more data on potential second-round inflation effects.