2026/03/06 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

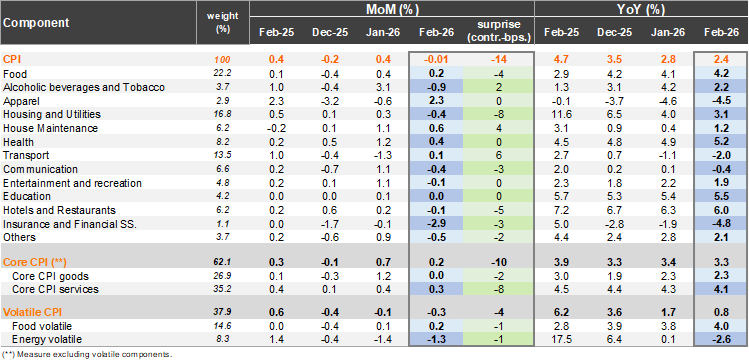

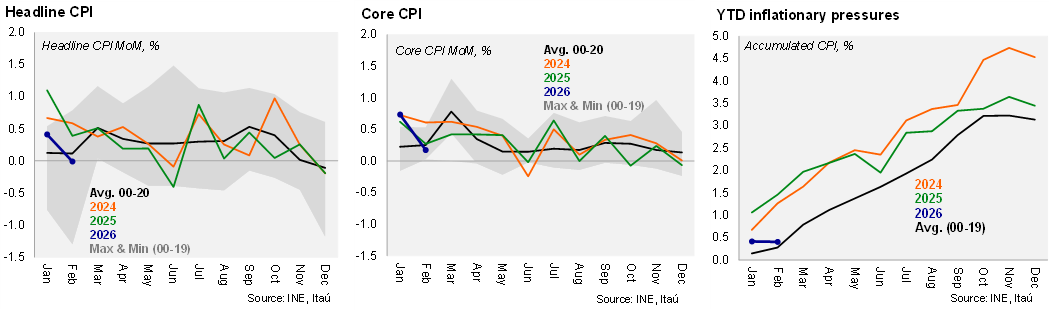

A downside surprise. According to the INE, consumer prices were stable between January and February, surprising the Bloomberg median and our call (both at +0.1%) to the downside. The key downside drags to prices came from the expected electricity retreat (correcting for a pricing error last year) as well as the seasonal payback of condominium fees, lower gas (LPG) and domestic air travel. Apparel, food items, rent and interurban bus travel boosted price gains. In annual terms, inflation dropped 0.41pp from January to reach 2.4%, the lowest annual print since August 2020. Core CPI (ex-volatiles) pressures showed signs of easing with a 0.2% MoM increase (Itau +0.33%), leading to a 3.3% YoY print (down 0.10pp from January). Core inflation was explained by a flat monthly print for core goods, resulting in an annual variation of 2.3%, while core services increased by 0.3% MoM, consisting in an annual change of 4.1% (falling -0.17 pp. from January). Our preliminary forecast for inflation in March ranges between 0.4-0.5% (2.3% YoY).

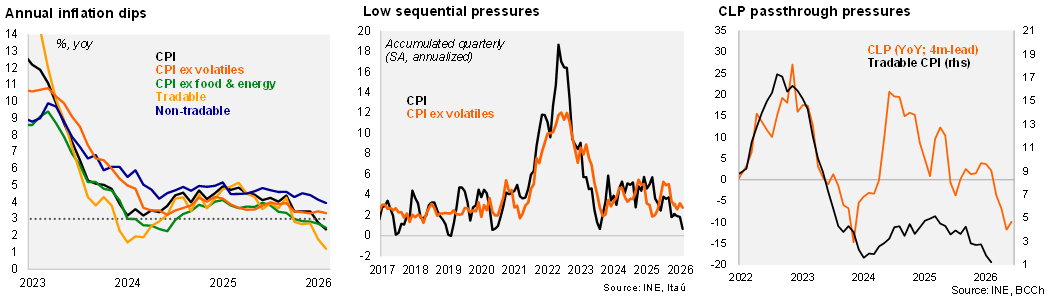

Low sequential pressures. At the margin, annualized inflation accumulated over the February quarter reached 0.7% (1.9% in line with 4Q), while core inflation sat at 2.7% (in line with 4Q). Volatile inflation dropped 0.9pp from January to 0.8%. Food inflation sits broadly stable 4.2%, while energy inflation fell 2.6pp from January to -2.4% YoY amid falling gasoline prices and the electricity price correction. We expect gasoline prices to register a hike in March (+2.4% MoM) and continue in months ahead (influenced by the geopolitical developments and CLP reaction). Excluding food and energy prices, inflation dipped 0.2pp to 2.5%. Nominal wage data for January eased by 1.2pp to 4.9% in January to the lowest rate since early 2021.

Our Take: Local factors support closing the monetary policy cycle with a 25bp rate cut later this month, but global developments may tilt the balance towards a hold. While private sentiment in Chile has shown sustained improvements over the last semester, activity dynamics have underwhelmed, with credit continuing to contract in real terms and the labor market failing to show significant improvements. On the inflation front we see contained sequential pressures, along with anchored medium-term price expectations, encouraging the Board to take the policy rate to the middle of the neutral rate range (4.25%). This was the last inflation print before the monetary policy meeting on March 24 (with the IpoM released the following day). Key domestic data ahead of the meeting include the BCCh’s analyst and trader surveys on March 10th and 19th, respectively, as well as the national accounts (March 18th). Prior to the conflict in the Middle East, we forecasted a final 25bp cut in March to a terminal rate of 4.25%, along with a neutral guidance. However, the global scenario is swiftly changing, with the swift rise in oil prices set to lift short-term inflation pressures before denting the medium-term growth outlook. With an estimated passthrough of 0.3pp of additional inflation per 10% oil price increase, the current global developments, if sustained, would be relevant. Our 2.8% yearend estimate considered an average WTI price of $60 per barrel (close to $ 85 currently). Overall, the global uncertainty spike merits caution and raises the odds of a pause in March.