2026/04/01 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

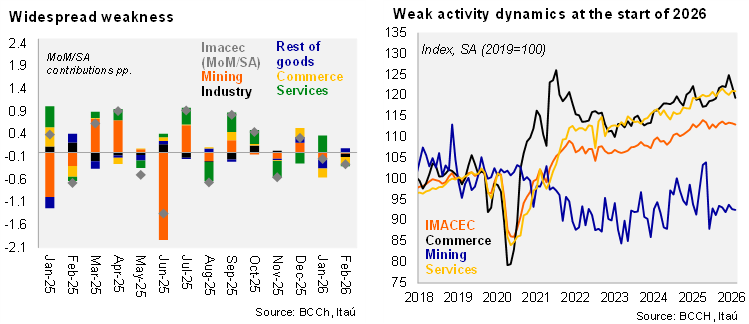

According to the Central Bank, the monthly GDP proxy (Imacec) for February posted a 0.3% YoY decline, well below market consensus (+1%), and marking a second consecutive negative print after the 0.5% contraction recorded in January. Non‑mining Imacec showed a similar pattern, falling 0.3% annually (-0.4% in January), reflecting broad-based weakness in the core components of activity. The overall result was mainly driven by a drop in goods production, including declines across industrial sectors, while the services sector partially offset this weakness. Sequentially, both total and non‑mining activity fell 0.3% MoM/SA, with the decline explained by weaker commerce and industrial activity. To meet the BCCh's 1Q26 growth forecast, March activity would need to rise by a substantial 3.6% YoY (our preliminary forecast points to a modest 0%-0.5% increase), a pace that appears difficult to achieve given recent momentum. According to our estimates, this is the weakest start to the year since 2017 (which was affected by a mining strike).

At the margin, activity continues to lose pace. Total activity posted a 0.3% QoQ/SAAR decline in the quarter ending in February (+0.8% in January; +2.1% in 4Q25), with non-mining activity posting a similar performance.

Our view: The latest figures confirm the weak activity start to the year and reinforce the downside bias to growth forecasts. Utilizing data from the February rolling quarter, the growth carryover for 2026 sits at 0.1%. Credit dynamics remain weak, with total bank loan growth holding at 2.2% YoY (nominal), unchanged from January, pointing to subdued demand. The labor market remains soft, with stagnant employment and slowing wage growth reinforcing downside risks. The weak activity data through February precedes the potential dent derived from the global oil price shock and tighter global financial conditions. In fact, private sentiment in March already showed signs of a deterioration. The March IMCE business sentiment (the first since the onset of the Middle East conflict) dropped 1.9 points to 50.4, whereas the non-mining breakdown fell 2.2 points to 47.2. Consumer sentiment dropped from 45.1 points to 43.6 in March. We see 2026 GDP growth at 2.1% (from 2.5% in 2025). While near‑term growth risks are tilted lower, the investment pipeline continues to progress, preserving a constructive medium‑term outlook.