2026/05/08 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

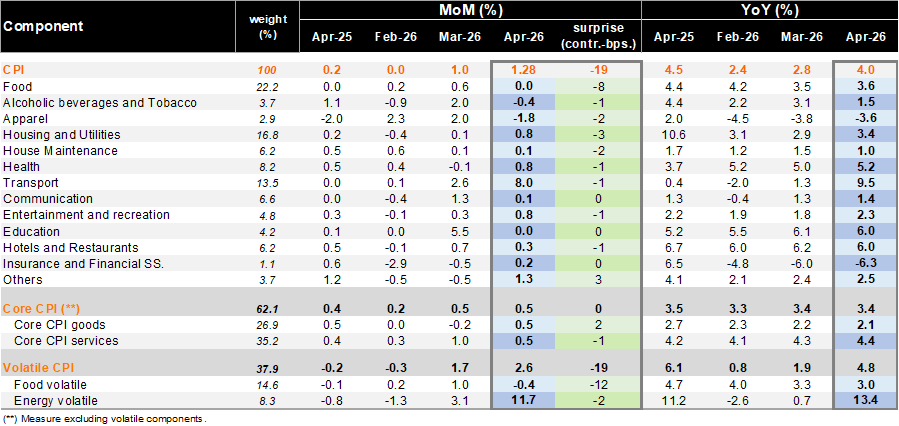

According to the INE, Consumer Price Index (CPI) rose by 1.28% MoM in April, below our call (1.46%), the Bloomberg median (1.5%), and breakevens (1.61%). As expected, fuel prices were a major driver to the monthly gain: gasoline prices increased 25.3% while diesel prices rose 45.7% both contributing 0.97 pp. to the headline monthly advance. Core CPI (ex-volatiles) increased by 0.5% MoM, driven by a 0.5% MoM rise in Core goods, while Core services did so by 0.4% MoM.

On an annual basis, headline inflation rose to 4.0%, up 1.12 pp. from March. Core CPI (ex-volatiles) increased to 3.4% YoY, rising 0.03 pp. from March. Core goods rose by 2.1% (down -0.05 pp. from March), while Core services did so by 4.4% (rising 0.09 pp. from March). Excluding food and energy, inflation stood at 2.8% YoY (-0.1 pp).

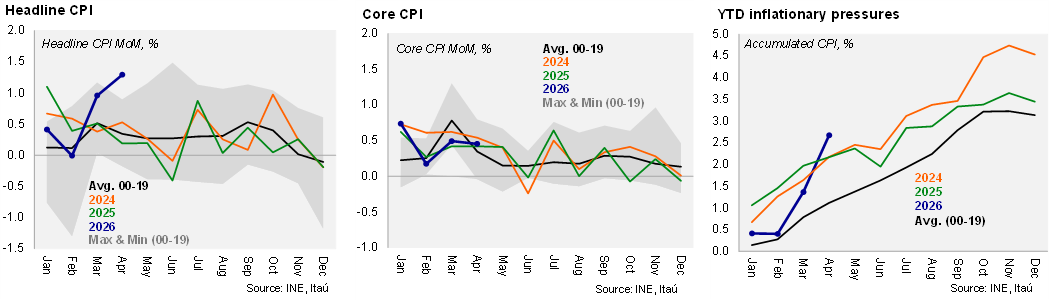

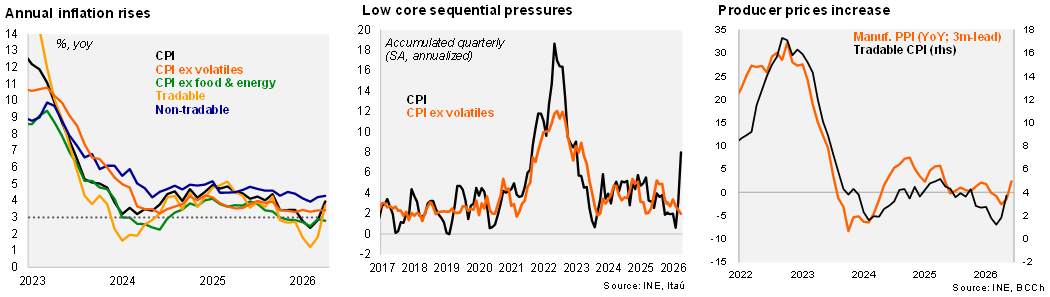

At the margin, annualized inflation accumulated over the April quarter jumped to 8% (vs. 3.2% in 1Q; highest since late 2022), while core inflation averaged a still contained 2.0%. Core goods ticked up at the margin (3.2% annualized) while services dipped to 1% annualized over the quarter.

Our Take: The lion’s share of the monthly increase was driven by fuels along with one-off declines in certain goods and services. Importantly, core inflation was in line with our call and the analyst survey median. In our view, the print reduces pressing concerns of a faster and broader pass-through of higher domestic fuel prices, for now. As such, market-implied pricing for hikes later this year, are likely to moderate, especially in the context of weaker than expected activity and a deterioration in the growth outlook. In any case, the downside surprise contrasts with upside inflation surprises we’ve seen recently elsewhere in the region. Our preliminary inflation forecast for May is between 0.3-0.4%, to be released on June 8, prior to the June 16 Monetary Policy Meeting. BCCh communication is likely to maintain a hawkish tone. Our base case is for the BCCh to remain on hold at 4.5% for the rest of the year. The next Analyst Survey is due May 12.