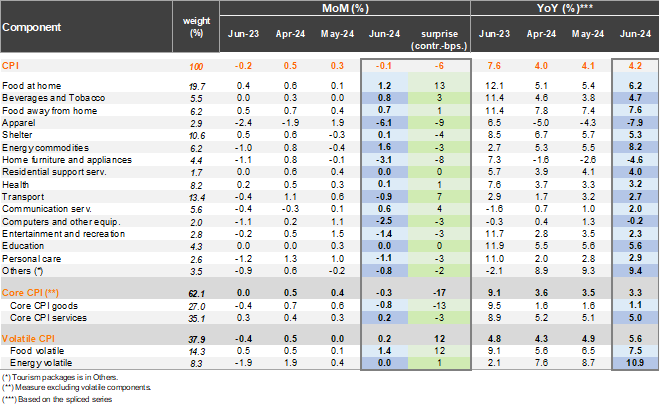

Consumer prices fell by 0.1% MoM in June, below both the both the Bloomberg market consensus and our call (0.0%), while in line with the implicit June CPI print in the 2Q24 IPoM. Key upside drivers in the month came from the food and non-alcoholic beverage division (+1.3%; +29bp contribution). Additionally, rising electricity prices (from the distribution front) led to an expected 7.2% monthly rise (+16bps). Notable drags came from falling gasoline prices (-2.2%; -8bps) and international air travel (-11%; -6bps), along with cyberday linked divisions such as apparel (-6% and -17bps) and the household equipment and maintenance (-2.2%; -13bps). Downside surprises to our call came from rent and certain food items. Annual inflation in the reference series rose to 3.8% (3.4% previously). Core inflation fell 0.2% in the month (IPoM: +0.1%), leading to an annual variation of 3.2% (reference series; 3.5% in May). Separately, as we had anticipated, a technical note from INE clarifies that the current electricity subsidy will not be considered in the price collection process as it does not directly modify the rate on electricity consumption.

Electricity prices lift services. Tradable prices fell 0.2% MoM (as cyberday dragged goods inflation down). Nevertheless, the annual tradable variation rose by 0.4pp to 3.2% YoY. The CLP remains 15% weaker than one year ago, supporting upside tradable inflation pressures during 2024. Food prices gained 1.3% MoM, and was up 1.1pp to 5.8% YoY. Separately, energy prices were flat in the month, but rose 2pp to 10.8% YoY as the electricity price increases offset falling gasoline. Non-tradables increased 0.3pp to 4.5% (reference series), with services at 4.8% (4.2% previously). At the margin, we estimate that inflation accumulated in the quarter was 4.2% (SA, annualized), down from 5.4% in 1Q24 (but up from 3.3% in 4Q23). Meanwhile, core inflation reached a lower 3.0% (SA, annualized, 4.5% in 1Q24 and 2.6% in 4Q23).

Our take: Headline inflation pressure will continue to rise as electricity price adjustments continue and pass-through from tradables trickles in. Although the distribution component of electricity rates already had a first increase in June, we expect a first relevant jump in the generation and transmission components in July. Furthermore, in July, certain price drops that occurred due to cyberday should be reversed. Overall, we expect inflation to end the year well above our 4.1% call. In this context, we still expect the Central Bank to lower the policy rate by 25bp to 5.5% in its July 31 meeting and then and enter a prolonged pause. INE will publish July’s CPI on August 8, which we estimate at +0.6-0.7%.