2026/06/24 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

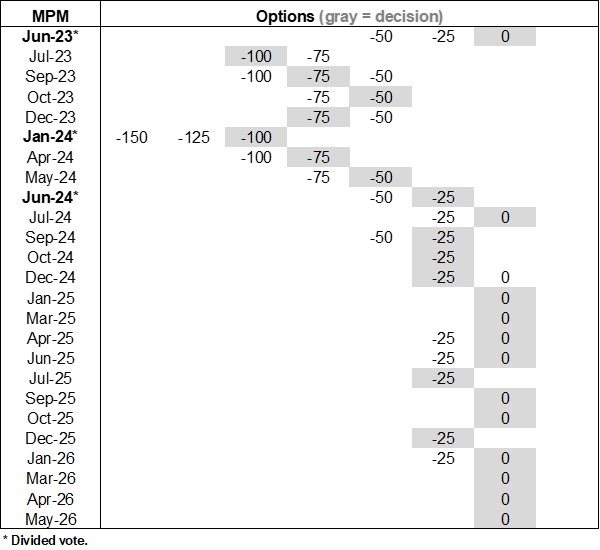

At the June meeting, the BCCh Board assessed that, although macroeconomic uncertainty remained above usual levels, inflation dynamics had largely unfolded as anticipated, with the outlook broadly unchanged and two-year ahead expectations still anchored at the 3% target, pointing to a more balanced inflation risk outlook. Members viewed the recent agreement between the United States and Iran as positive insofar as it reduced the likelihood of extreme oil price scenarios, although they stressed the need to monitor subsequent negotiations and the pace at which global oil supply normalizes.

Amid the heightened uncertainty, the Board emphasized that monetary policy credibility requires the same degree of caution in response to favorable news as to adverse shocks. This reinforced the importance of maintaining a meeting-by-meeting, data-dependent approach. Against this backdrop, all members judged that keeping the policy rate at 4.5% was the only appropriate course of action, considering that declining inflation risks reduced the need for a more contractionary stance, while signs of potential economic weakness remained tentative. They also underscored the need to carefully assess how domestic demand would respond to a more favorable external environment, alongside other internal drivers of spending. All Board members agreed that considering alternatives to holding the policy rate unchanged was not appropriate at this meeting.

Our Take: Our baseline scenario considers rates remaining on hold at 4.5% for the foreseeable future. The combination of still-elevated headline inflation and contained core dynamics supports a prolonged pause, as the central bank monitors second-round effects and expectations. With oil prices falling and inflation having accumulated several downside surprises, the urgency of additional tightening has reduced, while expectations of rising rates abroad and the supply-shock nature of the activity slowdown limits the appeal of lowering rates. The next monetary policy meeting will take place on July 28.