2026/05/29 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

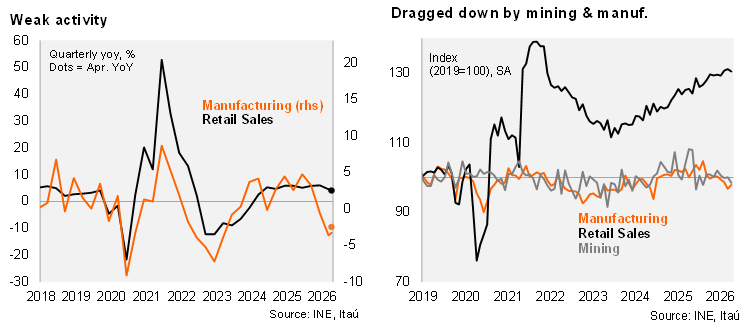

Retail sales and manufacturing surprised to the downside in April. According to Chile’s National Statistics Institute (INE), retail sales grew 4.1% YoY, falling short of both the Bloomberg consensus (4.8%) and our forecast (4.9%). Growth was supported by diversified consumption goods, new vehicles, and auto parts, which increased by 6.8%, 15.6%, and 10.0%, respectively. However, in seasonally adjusted terms, retail sales declined by 0.5% MoM, reversing the 0.3% gain recorded in March.

Manufacturing output contracted 2.5% YoY, slightly better than market expectations (-2.8%) and our forecast (-3.0%), but still indicative of weak underlying momentum. The decline was largely driven by a 7.7% contraction in food production. On a sequential basis, however, manufacturing rebounded by 1.1% MoM/SA after a 1.9% drop in March. Mining output fell sharply by 9.0% YoY, reflecting a high base of comparison and lower ore grades at major producers. In seasonally adjusted monthly terms, mining declined 1.6% (vs. +0.2% in March). As a result, total industrial production contracted 4.7% YoY and edged down 0.2% MoM (seasonally adjusted).

Activity at the margin still shows limited signs of recovery. For the quarter ending in April, industrial production contracted 3.1% YoY (vs. -2.0% in 1Q26), while real retail sales grew 4.7% YoY (broadly in line with 4.6% in 1Q26). On a sequential basis, manufacturing contracted 8.8% QoQ/SAAR (vs. -7.0% in 1Q26), while mining shrank 5.7% QoQ/SAAR (vs. -3.3% in 1Q26), pointing to persistent weakness in cyclical sectors. Real retail sales gained some traction, expanding 4.4% QoQ/SAAR (up from 2.7% in 1Q26), but remain well below the stronger momentum seen in previous years.

Our take: Overall, the data reinforce a narrative of weak activity at the margin and consolidate downside risks to our 2.1% GDP forecast for this year. We have revised our April Imacec estimate to a 1.0% YoY contraction (+0.5% YoY for non-mining; to be published Monday, June 1). External headwinds—including tighter global financial conditions and higher oil prices—continue to weigh on the near-term outlook. That said, a stronger investment pipeline, together with policy efforts aimed at unlocking private investment, should help underpin a more sustained recovery once current cyclical headwinds begin to fade.