2026/06/01 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

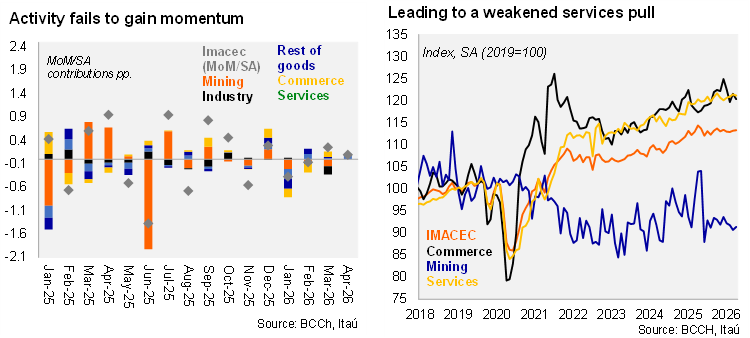

According to the central bank, the April monthly GDP proxy (Imacec) posted a year-over-year contraction of 1.2%, significantly below the market expectation of -0.1%, but closer to our forecast of -1.0%. The non-mining Imacec recorded a modest annual expansion of 0.4% (Itaú: 0.5%). The overall results were explained largely by a sharp decline in mining activity (down 12% YoY). Additional negative contributions came from the rest of goods and manufacturing sectors, affected in part by weaker fishing activity. Growth support from commerce and services weakened with retail activity growing 2.1% YoY (4.7% in March)—led by strong automotive sales—and services expanding 0.8% YoY (2.1% in March), particularly driven by personal services such as healthcare, though this was partially offset by weaker business services.

Sequentially, activity has plateaued. Total activity increased by a mild 0.1% Mom/SA while the non-mining component remained flat compared to the previous month. Likewise, in the quarter ending in April, total activity posted a null QoQ/SAAR variation (-1.3% in 1Q26), with non-mining activity posting a 0.9% QoQ/SAAR rise (-0.5% in 1Q26).

Our Take:Overall, these figures reinforce signs of short-term weakness in activity and highlight downside risks to a more sustained recovery, amid softer wage growth and limited job creation. We preliminarily expect May Imacec to come in between 0% and 0.5%. Carryover for the year (using the April quarter, SA) sits at 0.1%. Against this backdrop, we have revised down our 2026 GDP growth forecast to 1.5% (from 2.1%), reflecting weaker-than-expected activity at the start of the year, low statistical carry-over, and a still-fragile labor market weighing on consumption. At the same time, an adverse external environment (tighter financial conditions and higher oil prices) adds pressure in the near term. That said, we have raised our 2027 growth forecast to 3.1% (from 2.8%), as macro fundamentals remain supportive and investment dynamics are expected to improve. A stronger project pipeline and policy efforts to unlock private investment should underpin a more sustained recovery once current cyclical headwinds fade. Inflation is likely to remain elevated in the short term (4.5% this year), driven by energy prices, but contained core pressures and anchored expectations support a gradual convergence to target. In this context, the central bank is likely to remain cautious and data-dependent, keeping the policy rate at 4.5% for an extended period.