2026/03/18 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

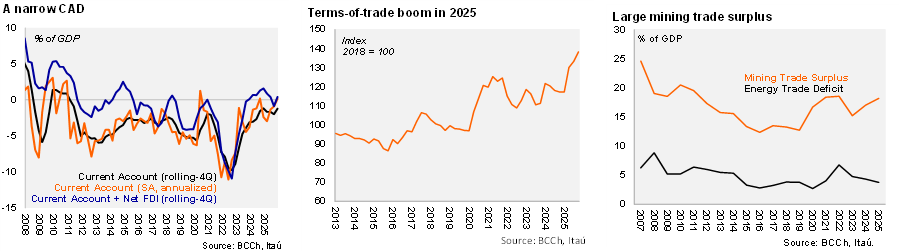

A USD 1.3 billion current account surplus was registered in 4Q25, a reversal from the USD 1.3 billion deficit in 4Q24 as the goods trade surplus boomed. Overall, the current account deficit in 2025 remained at 1.2% of GDP, in line with 2024, and the lowest since 2010. Between 2011 and 2020, the CAD averaged a tick below 4% of GDP. Net FDI fully financed the current account deficit last year. External debt sits at 74% of GDP (78% at the close of 2024), with the nominal annual increase of USD 32 billion mostly explained by public debt issuance.

A terms-of-trade surge closed the year. Exports of goods grew by 21% YoY in 4Q25 (12% in 2025), while imports rose by 8% (11% in 2025). On the mining front (+34% YoY in 4Q25), prices (+29% YoY) rather than volumes (+5% YoY) led the strong export close to 2025. The domestic demand outlook remained positive, with imports of capital goods rising 24% YoY in 4Q25 (and 25% during the full year). Imports of consumer goods slowed to 5% (10% in 2025). The services deficit narrowed at the margin amid a boom in tourism to Chile during 2025. With rising mining prices, the income deficit also increased (to USD 5.2 billion in 4Q25; USD 3.6 billion in 4Q24) amid favorable FDI returns.

Our Take: The mining outlook remains favorable, but the oil trade deficit is set to rise this year. The energy trade deficit came in a tick below 4% of GDP last year. If global energy prices were to remain at current prices going forward, the energy trade deficit could increase by around 2pp. Nevertheless, even if energy prices remain above last year, the current commodity price mix will likely still result in a current account balance that remains low in historical terms and well-financed.