2026/03/09 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

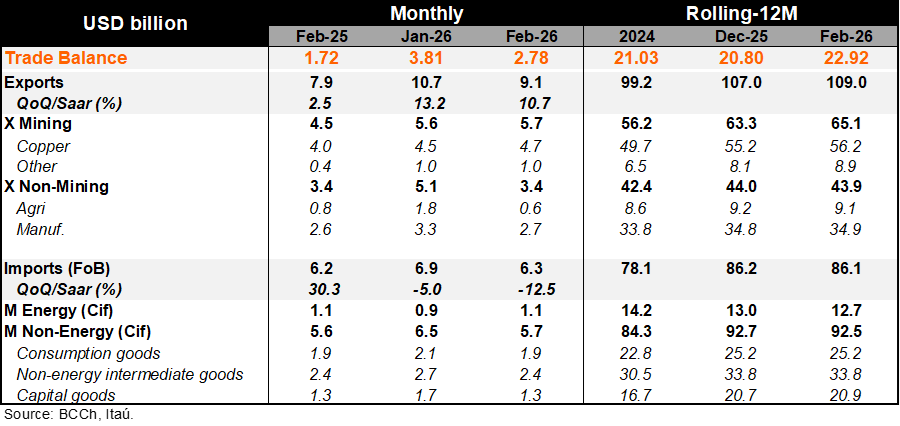

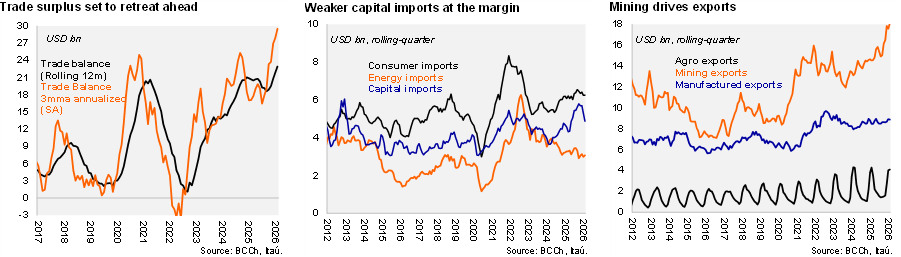

A trade surplus of USD 2.8 billion was recorded in February (Itaú: USD 2.7 billion; Bloomberg: USD 2.6 billion), lifted by mining and manufacturing while import dynamics remained contained. As a result, the rolling 12-month trade balance reached USD 22.9 billion (USD 20.8 in 2025; USD 21 billion in 2024). The annualized quarterly trade balance sits at a higher USD 29.5 billion as mining exports rebound and capital goods imports lose steam. Exports grew 15% year-on-year in February (8.5% in January), boosted by the 28% mining gain. Within mining, copper exports rose by 16%, meanwhile gold exports more than doubled over the last year to USD325 million, and lithium exports more than tripled USD 397million (highest since early 2023). Manufactured exports were up 5% (lifted by food, wine and chemicals). Agriculture exports shrunk, dragged by a halving of blueberry and cherry sales. On the import side, total imports rose by 3.5% YoY (-3.6% in January) with durable consumer goods leading the recovery (vehicles and mobile phones). Energy imports rose by a moderate 2.7% YoY yet remain at low levels and will swiftly rise as the middle east war drags on. Energy imports during the last quarter totaled USD 3.1 billion, while during the 2022 oil price shock, quarterly energy imports peaked at USD 6.1 billion. Meanwhile, capital goods imports were flat over twelve months, while retreating USD 0.8 billion from the last year’s cycle peak in October. At the margin, the downturn is linked to the automative industry given import frontloading ahead of a change to operating norms.

Our Take: The latest surge in oil prices will chip away at the record high terms-of trade. Prior to the war, we expected the trade surplus to exceed 6% of GDP this year. Chile’s energy trade deficit was a tick below 4% of GDP in 2025 (close to 7% in 2022). Higher global energy prices and risk off market sentiment (evident in the CLP unwind) have lifted inflation expectations. Yearend breakevens have risen by around 50bps over the last month to 3.2%. Our 2.8% inflation call considered average brent prices of USD 65 per barrel for the year. Our preliminary March CPI forecast sits in the 0.4-0.5% range, already incorporating a 3% gasoline price increase responding to the price increases registered since yearend. The passthrough to inflation is smoothed in Chile thanks to the fuel price stabilization fund (MEPCO) which adjusts prices on a three-week cycle. The BCCh will hold their Monetary Policy Meeting by the end of the month; prior to the conflict in the Middle East we were considering a final 25bp cut to a terminal rate at 4.25%, the center of the neutral rate range.