2026/06/08 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

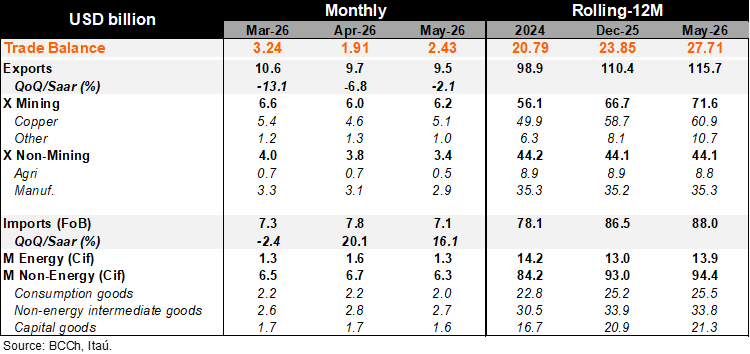

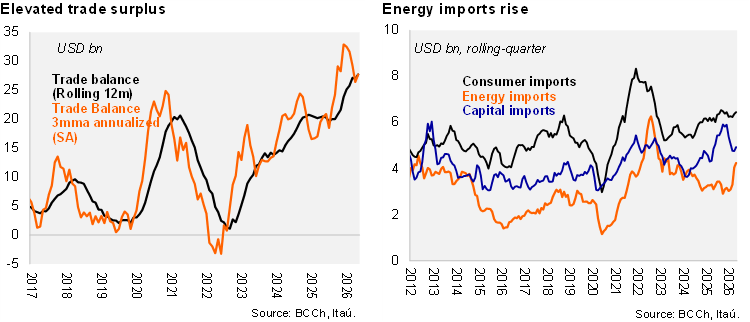

A trade surplus of USD 2.4 billion was recorded in May (Itaú: USD 1.8 billion; Bloomberg: USD 1.9 billion), lifted by a mining surge (14.7% YoY; reflecting prices) and firm manufacturing (4.4% YoY) while non-energy import dynamics were weak. As a result, the rolling 12-month trade balance reached USD 27.7 billion (USD 23.8 in 2025; USD 20.8 billion in 2024). The annualized quarterly trade balance sits at a similar USD 27.7 billion as mining exports rebound and capital goods imports lose steam. Total exports grew 9.3% year-on-year in May. Copper exports rose by 8.7%, meanwhile gold exports more than doubled over the last year to USD410 million, and lithium exports more than tripled USD 343million. Manufactured exports were up 4.4% (lifted by chemicals). Agriculture exports shrunk, dragged by weaker fruit dynamics. On the import side, total imports rose by a moderate 1.0% YoY as consumer goods imports slow and capital goods imports contracted for the first time since late 2024. Transportation related goods as well as machinery for construction and mining were key drags in the month. On the other hand, energy imports rose by 51.9% YoY as the conflict in the Middle East maintains pressure on oil prices. Energy imports during the latest quarter totaled USD 4.3 billion, while during the 2022 oil price shock, quarterly energy imports peaked at USD 6.3 billion.

Our Take: We expect a narrower current account deficit of 1.0% of GDP this year, driven by a stronger-than expected surplus during the1H26. While higher oil prices will push import values higher and widen the energy deficit, this is likely to be offset by resilient mining exports, underpinned by favorable price dynamics. The annual contraction in capital goods imports is likely to be transitory, although should be interpreted as another sign of concern in the context of persistently weaker activity. The CLP should remain volatile in the short term, sensitive to global risk and oil price swings, but the medium-term outlook remains constructive.