CHILE – An important step towards boosting long-term growth

2026/04/22 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

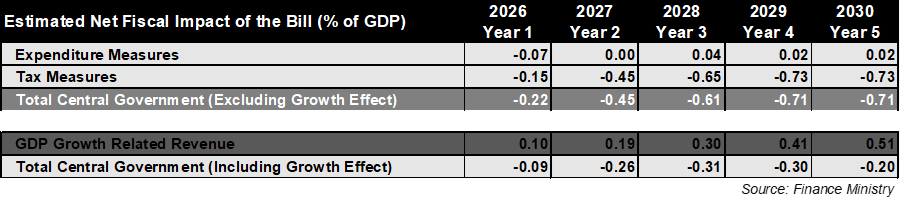

As widely anticipated, the Kast administration presented the National Reconstruction Bill, which includes more than forty measures aimed at boosting Chile’s potential growth, primarily through policies that strengthen private investment via tax cuts and regulatory streamlining. The bill acknowledges short term revenue losses, framing higher medium-term growth along with expenditure cuts as the main mechanisms to stabilize the fiscal accounts.

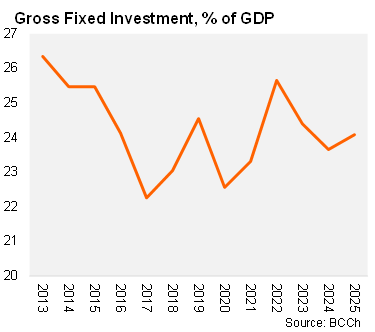

For context, Chile’s tax system has undergone several major overhauls since 2014 that have increased the cost of capital, reduced the economy’s competitiveness, and ultimately fallen short of revenue expectations. Over this period, investment as a share of GDP has gradually declined.

Enhancing Chile’s tax competitiveness comes with an officially estimated annual revenue loss of roughly USD3 billion by 2030 (around 0.7% of GDP). When accounting for the full set of tax measures, the Budget Office estimates the revenue gains generated by the bill would amount to 0.5% of GDP by 2030, resulting in a net fiscal impact of -0.2% of GDP.

The bill’s main tax measures include:

· A gradual reduction of the corporate income tax rate from 27% to 23% by 2029 for large companies. The corporate tax rate is scheduled to decline from 27% to 25.5% in 2027, 24% in 2028, and 23% thereafter.

· Full reintegration of the tax system, gradually eliminating the requirement to repay the corporate tax credit and simplifying the corporate tax regime.

· A 25-year tax stability statute for domestic and foreign investments exceeding USD 50 million, including protection against future tax changes and, in the case of mining, against changes in royalties and mining licenses.

· Elimination of the 10% flat tax on capital gains from listed securities, restoring their treatment as non-taxable income to boost liquidity and depth in financial markets.

· A Tax credit for formal employment, equivalent to up to 15% of wages for lower-income workers (up to 7.8 UTM, slightly above the minimum wage), gradually decreasing to zero at 12 UTM, focused on SMEs and formal job creation.

· A one-year VAT exemption on sales of new homes.

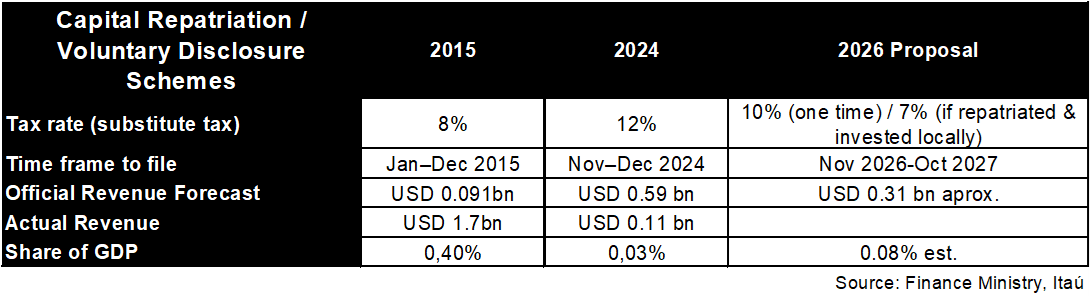

Big miss in the last capital repatriation and voluntary disclosure scheme

Regarding expenditure, the bill also seeks to mitigate the risk of fiscal slippage in key areas. The measures mentioned below complement the spending cuts announced at the start of the administration. Specifically, the bill proposes:

· A two-year freeze on the entry of new institutions into the tuition-free higher education system.

· Stricter integrity rules for medical leave in the public sector.

· Elimination of the SENCE tax credit, due to demonstrated low effectiveness.

· Increase in voluntary retirement slots in the public sector (from 2,200 to 6,000).

On streamlining investment, the bill proposes:

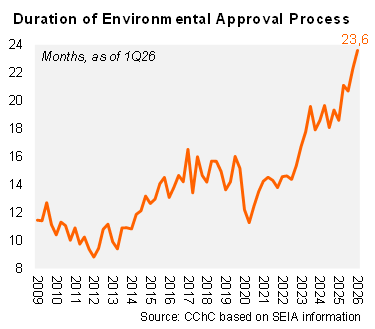

· Reduction of the validity period for sectoral permits from two years to six months.

· Comprehensive reform of the Environmental Impact Assessment System (SEIA), including fewer review stages, limits on administrative challenges, binding deadlines for appeals, and a voluntary special environmental assessment regime.

· Compensation mechanism for project developers when a favorable permit (RCA) is overturned by the courts.

· Streamlining of infrastructure, energy, mining, and aquaculture projects, including measures related to micro-relocations and non-use patent rules.

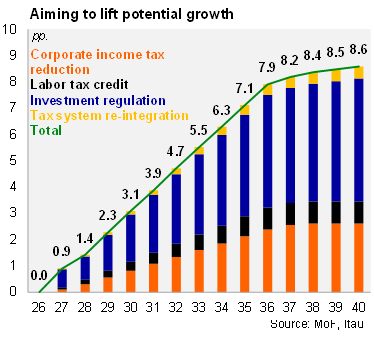

According to official forecasts, the bill’s measures are projected to increase the GDP level by 2.3 percentage points by the end of the Kast administration (2029), reaching a cumulative gain of 8.2 pp. over a ten‑year horizon. This impact is driven by four main channels: (i) Gradual reduction of the corporate income tax; (ii) Formal employment tax credit; (iii) Tax reintegration (iv) Investment streamlining measures and tax invariability provisions. Furthermore, the MoF states that these estimates are based on conservative assumptions and do not incorporate potential synergies across measures, which could lift trend growth to levels closer to 4%.

Our view:

- The governing coalition remains slightly short of a majority in both chambers and will therefore need to negotiate to secure legislative approval. Government officials have emphasized the importance of passing the bill ahead of the 2027 budget discussion (September 30), as tax reforms typically require lengthy debates, particularly at the committee level. The bill will be discussed in the lower house’s finance, labor, and environmental committees.

- The Autonomous Fiscal Council’s view on the bill’s fiscal impact will be key in the legislative discussion.

- Demonstrating swift progress on this year’s spending cuts will be critical for restoring fiscal credibility. Upon taking office the administration instructed ministries to reduce expenditures by 3% (approximately USD3 billion), alongside an additional USD1 billion in cross-ministry cuts. Together, these measures would amount to spending reductions of roughly 1.2% of GDP this year. Delivering on these cuts would help offset the bill’s projected revenue losses and facilitate legislative approval.

- Permanent tax credits for formal employment in SMEs offset the sharp rise in labor costs in recent years. Since 2022, the nominal minimum wage increased by roughly 50%, the workweek has been reduced, and higher employer pension contributions are being phased-in, materially raising labor costs. In practice, this measure would reduce the effective corporate income tax rate below 23%.

- The proposal has the potential to further support the ongoing investment cycle and raise Chile’s potential GDP.

- In our view, the Bill will not alter the need to issue the full authorized amount of debt this year (USD 17.4 billion).

- The MoF must decree its medium-term fiscal plan by June 9th.

Andrés Pérez M.

Vittorio Peretti

Andrea Tellechea Garcia

Ignacio Martínez