2026/04/30 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

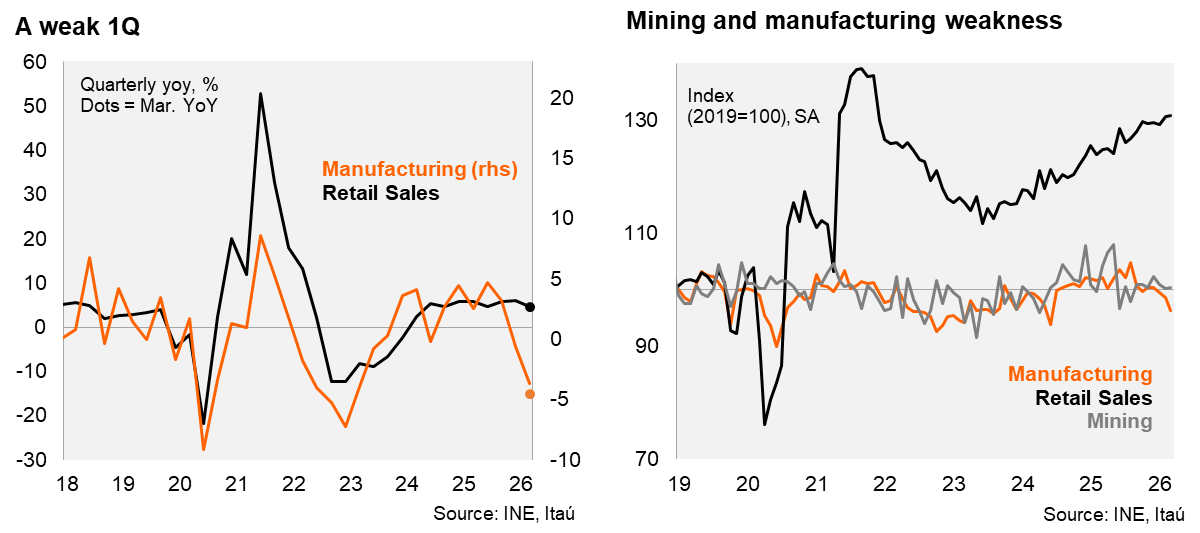

Manufacturing and mining dragged activity down in March, while retail sales growth lost momentum. We estimate the monthly GDP proxy (IMACEC) contracted by 0.5% YoY in March (to be released on May 4), resulting in a 0.5% decline during 1Q26 (BCCh: +1%; +1.6% in 4Q25). According to INE data, real retail sales grew by 4.6% year over year, below the Bloomberg median (4.9%) and our forecast (5%). The strongest positive contributions came from auto parts and accessories (12.2%), miscellaneous consumer goods (5.2%), and electronic products (5.1%). On a seasonally adjusted basis, retail sales edged up 0.1% MoM/SA, slowing from the 1.0% increase recorded in February. The sequential deceleration takes place as tourism inflows to Chile have declined materially and the labor market maintains slack. Meanwhile, manufacturing production contracted by 4.5% annually, well below market expectations (Bloomberg consensus: -1.2%; Itaú: -2.5%), largely driven by an 11.9% year‑over‑year decline in food processing. Sequentially, manufacturing fell by 2.3% MoM SA (from -0.9% in February). Still, manufacturing weakness seems broad-based. Mining output also fell 3.7% year over year, although it posted a modest 0.2% MoM/SA increase. As a result, overall industrial production declined by 3.4% annually (-0.9% MoM SA).

During 1Q26, industrial production contracted by 2.1% YoY (-1.1% in 4Q25) and real retail sales growth slowed from 6% in 4Q25 to 4.6%. Sequentially, manufacturing contracted 7.8% QoQ/SAAR (similar to the drop in 4Q25) and mining shrunk 3.1% QoQ/SAAR (+5.6% in 4Q25). Real retail sales momentum slowed to 2.3% QoQ/SAAR, from 8.6% during the final quarter of last year, and the slowest growth pace since 3Q24. If activity remained at the 1Q levels (SA) for the rest of the year, manufacturing, mining and retail sales would respectively change by -3.4%, -1.1%, and +2.8% this year.

Consumer and business confidence take a hit in April. According to the monthly IMCE index, business confidence slipped for the third consecutive month, falling to 49.2, slightly below neutral (50), the lowest level since end-2025 (45.28). The index hit a cyclical peak of 52.3 in February. The decline at the margin was mainly driven by a deterioration in future expectations of the Chilean economy. Consumer confidence, as measured by IPEC, crashed in April by nearly 10pp to 34.2, from 43.6 in March, the greatest monthly decline since the 2010 earthquake. Consumer confidence had also peaked at the start of the year (47.0 in January), the highest since 2019, and has since fallen every month. The sharp deterioration was driven by concerns on the economic outlook, especially inflation and the labor market.

Our take: Our 2026 GDP growth forecast is 2.1%, although weak activity tracking and additional short-term headwinds (energy costs and fiscal cuts) pose downside risks. The assumption of a transitory oil price spike, elevated metal prices and a push to unlock investment projects support our view of an acceleration over our forecast horizon. Revised national accounts data (May 18) may bring relevant updates. Overall, the central bank faces an unenviable task. Recent BCCh communication underscores a deliberately cautious, data-dependent stance, balancing higher inflation against softer activity. With price pressures stemming largely from external and cost shocks, the Central Bank’s priority remains anchoring expectations, rather than reacting mechanically to headline volatility. Encouragingly, while trader and analyst surveys show a sharp pickup in short-term inflation expectations, the two-year horizon remains essentially at the 3% target.