2026/05/04 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

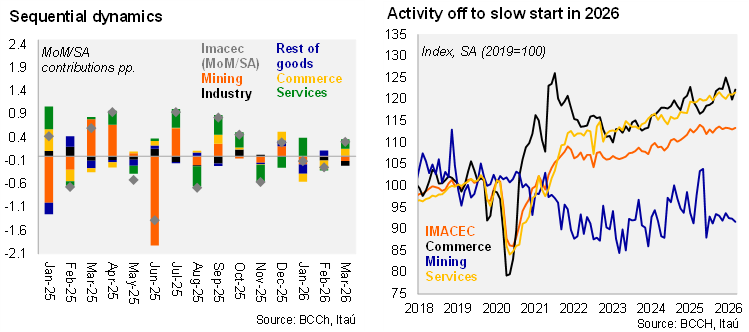

According to the Central Bank, the monthly GDP proxy (Imacec) for March fell by 0.1% YoY (-0.3% in February), in between the Bloomberg median (+0.5%) and our -0.5% call. Non‑mining Imacec rose by 0.9% annually (-0.3% in February). March had one additional working day this year. The overall result was mainly driven by a drop in goods production with mining falling by 6.5% YoY and industrial sectors down 2.6% (dragged by weakness in the fishery sector). The services sector (+2.1% YoY), aided by health, and commerce (+5.1% YoY), lifted by machinery and equipment and grocery sales, partially offset weakness elsewhere in the economy. During 1Q26, activity contracted 0.3% YoY (+1.6% in 4Q25; IPoM: 1%), the first decline since 2Q23, and pulled down by the production of goods (-3.7% YoY). Consumption growth slowed to 1.4% (7.2% in 4Q25) and services cooled to 2.1% YoY (3.6% in 4Q25). Overall, non-mining activity grew a mere 0.1% (2.6% in 4Q26).

Sequentially, activity closed the 1Q with a partial recovery. Total activity rose by 0.3% Mom/SA and non-mining was up 0.5%. Nevertheless, total activity posted a 0.6% QoQ/SAAR decline in the first quarter (+2.1% in 4Q25; +2.1% in 4Q25), with non-mining activity posting a 0.1% QoQ/SAAR contraction (+2.1% in 4Q25). If activity were to remain at 1Q levels (SA) for the remainder of the year, 2026 growth would come in at 0.1%.

Our Take: Weak activity tracking and additional short-term headwinds (energy costs and fiscal cuts) pose downside risks to our 2.1% GDP growth forecast for the year. Revised national accounts data (May 18) may bring relevant updates to the economic standing of the economy at the start of the year. We preliminarily see the April Imacec as being unchanged from its 2025 levels. While some of the slowdown may be attributed to transitory sector specific challenges (fishing), the broader economy has lost momentum. Additionally, the data is yet to reflect how factors such as the sudden consumer price surge during 2Q26, the sharp decline in private sentiment and the start of fiscal spending adjustments affect growth dynamics. The central bank’s meeting-by-meeting approach will need to weigh-up weaker activity dynamics and labor market slack with a cost driven inflation increase. Our baseline scenario considers rates on hold at 4.5%, contingent on the two-year inflation expectations remaining anchored. On May 8, the April CPI data will likely show a large 1.5% monthly increase, lifted the annual variation by 1.4pp to 4.2%