2026/04/07 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

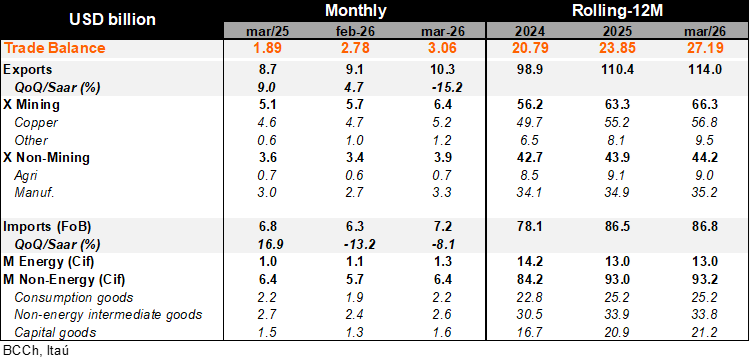

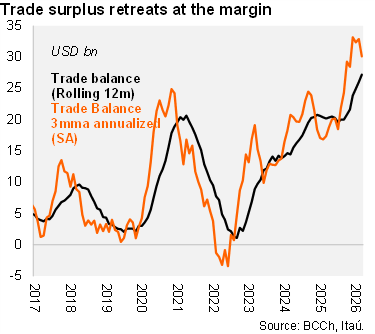

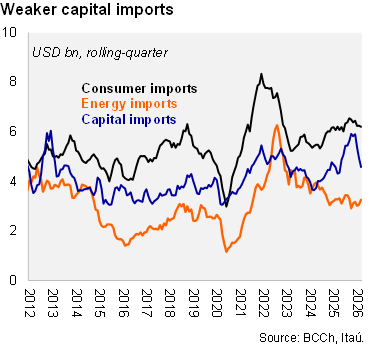

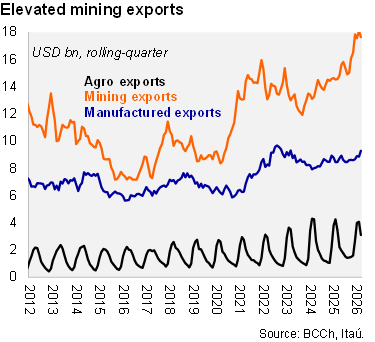

A trade surplus of USD 3.1 billion was recorded in March (Itaú: 3.0 billion; USD 1.9 billion in March 2025), lifted by mining and manufacturing while import dynamics reflect a tick up in fuels. As a result, the rolling 12-month trade balance reached USD 27.2 billion (USD 23.9 in 2025; USD 20.8 billion in 2024). Exports grew 14% year-on-year in 1Q26 (22% in 4Q25), boosted by the 22% mining gain. Within mining, copper exports rose by 13% in 1Q26, while gold (USD 1.2 billion), silver and lithium (USD 1.1 billion) exports all roughly doubled over one year. Manufactured exports were up 10% in the quarter, supported by chemical and food sales. Separately, total imports rose by 1.5% YoY in 1Q26 (8% in 4Q25) with durable consumer goods broadly flat over one year. Capital goods imports remain elevated yet grew at a slower 6.2% YoY in the quarter (24% in 4Q25), lifted by machinery and equipment, while vehicle imports shrunk. While overall energy imports were broadly flat between 1Q25 and 1Q26, gasoline and diesel imports surged by a respective 30% and 81% YoY in March, reflecting higher global energy prices, in turn, driven by the Middle East conflict.

Our Take: The surge in international oil prices will chip away at the record high terms-of trade levels present prior to the war. Nevertheless, trade dynamics surprised to the upside in 1Q. The energy trade deficit reached USD 13 billion last year and could rise by around 50% this year. We expect the trade surplus to tick down to 6% of GDP (7% in 2025) as metal prices remain favorable. Overall, we see the CAD rising from 1.2% of GDP last year to a still low 1.7% this year.