2026/05/18 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

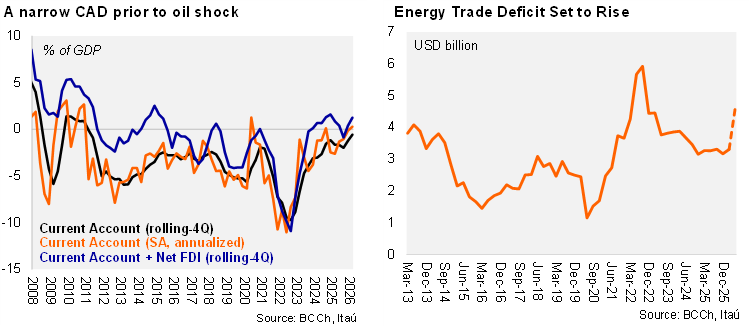

A USD 1.9 billion current account surplus was registered in 1Q26 (1.9% of GDP), a reversal from the USD 0.3 billion deficit in 1Q25, amid a large trade surplus for goods. The surplus in 1Q was a tick above our USD 1.7 billion call and the Bloomberg median of USD 1.4 billion. Overall, the rolling-4Q current account balance came in at a deficit of 0.6% of GDP (-1.2% in 2025). The CAD averaged a tick below 4% of GDP during 2011 and 2020. Net FDI fully financed the current account deficit over the last year. External debt sits at 75.9% of GDP (75.3% at the start of 2025), explained primarily by transactions in the Government and Banking sectors.

A terms-of-trade surge prior to the oil shock. The trade of goods surplus reached USD 9.6 billion (USD 6.3 billion in 1Q25) as exports rose by 15% YoY and imports growth slowed to 2.9% YoY. The key export driver was mining, rising by 23% YoY, as prices gained 28% over one year. On the import front, the volume of capital goods continued to rise at a double-digit rate. Meanwhile, energy goods prices continued to contract on an annual basis (-4.5% YoY), a scenario that is set to revert sharply in 2Q26. The services deficit was broadly steady at USD 2.0 billion. With rising mining prices, the income deficit also increased to the highest on record (USD 6.0 billion from USD 4.6 billion in 1Q25) amid favorable FDI returns.

Our Take: The mining outlook remains favorable, but the oil trade deficit is set to rise. Nevertheless, even with an adjustment in energy prices, the current commodity price mix will likely still result in a current account balance that remains low in historical terms (1.7% of GDP) and well-financed.