2026/06/08 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

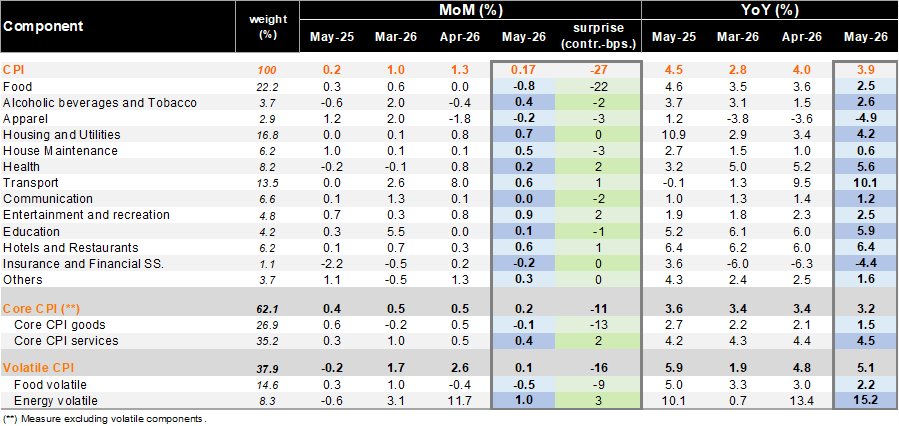

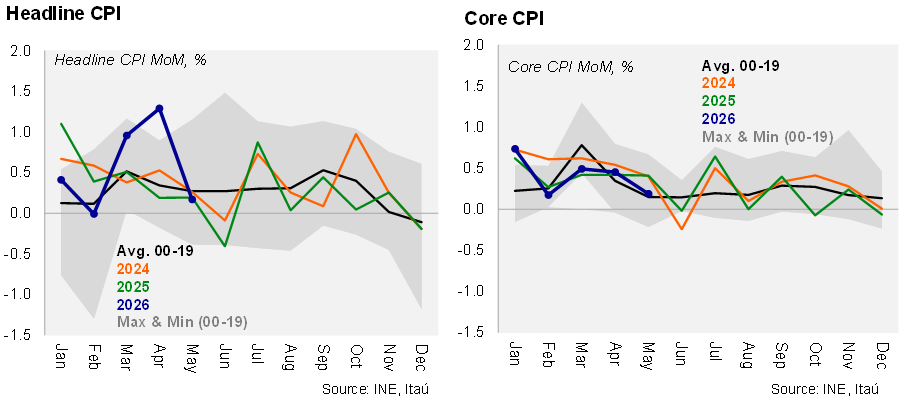

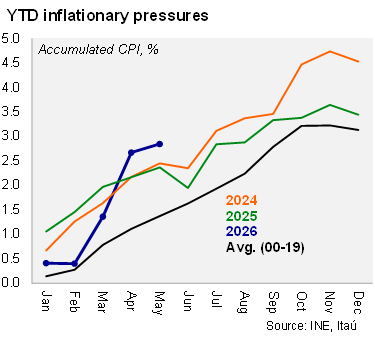

According to the INE, Consumer Price Index (CPI) rose by 0.17% in May, well below the Bloomberg median and our call (both at 0.4%). Cumulative inflation in the year reaches 2.8%. Among the items with notable MoM increases, the following stood out: Beef meat (2.7%; 0.06 pp. of contribution), Food Purchased in Restaurants, Cafés, and Similar (1.0%; 0.05 pp. of contribution) and International Air Transport (10.0%; 0.05 pp. of contribution). On the downside, the most significant price drops were observed in: Bread (-4.0%; -0.08 pp. of contribution), Intercity Bus Transport (-9.1%; -0.03 pp. of contribution) and Lemons (-17.2%; -0.03 pp. of contribution). Core CPI (ex-volatiles) registered a 0.2% MoM increase, suggesting limited pass-through of recent fuel price increases. The Core results were driven by a -0.1% MoM drop in Core goods, while Core services increased by 0.4% MoM.

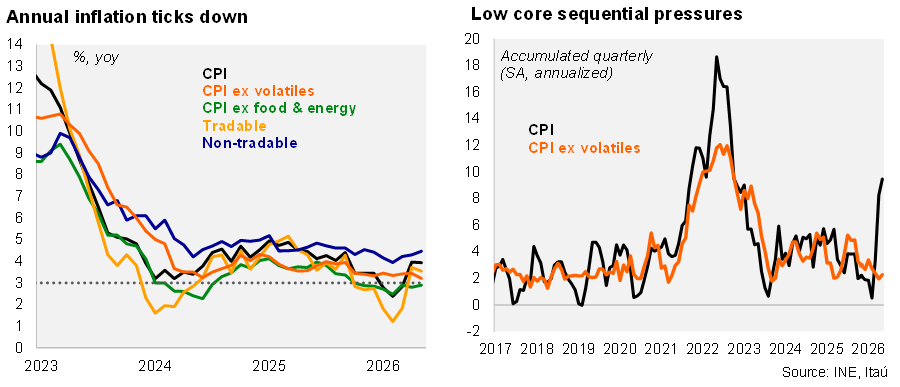

In annual terms, headline CPI returned to the BCCh’s tolerance range. Headline results translate to a year-on-year variation of 3.9%, down -0.03 pp. from April. Core CPI (ex-volatiles) registered a 3.2% YoY, falling -0.23 pp. from April, where Core goods rose by 1.5% YoY (down -0.65 pp. from April) and Core services registered a 4.5% increase (rising 0.08 pp. from April).

At the margin, headline CPI rose sequentially to 9.5% annualized in the quarter, mainly reflecting the March-April increases, yet core inflation remained muted at 2.3%.

Our take: May’s results suggest that the lion’s share of the fuel-related inflationary shock is concentrated in CPI’s energy component, with contained second-round effects so far. The benign May print takes place in the context of weak activity and ongoing labor market slack, helping to contain demand-side inflationary pressures. We forecast year-end inflation at 4.5%, slightly above market-pricing (4.4%). with a preliminary forecast for June of -0.2% MoM (affected by widespread sales events). The benign May print, along with anchored medium term inflation expectations, support the view that the Central Bank of Chile (BCCh) will remain on hold at 4.5% at the end-June Monetary Policy Meeting. Our baseline scenario assumes the monetary policy rate will remain unchanged through year-end. The BCCh will publish the results of its analyst survey on Wednesday where we expect the view of a transitory inflation shock to persist, accompanied by another downgrade to 2026 GDP growth (median currently at 2.0%, down from 2.6% in the February survey).