2026/06/17 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

The June 2026 IPoM portrays a macroeconomic environment characterized by a temporary stagflationary mix, where growth has weakened due to sector-specific supply shocks while inflation has risen on the back of higher global oil prices. The BCCh assesses the recent deterioration in activity as largely transitory and concentrated in natural resource sectors, whereas the uptick in inflation reflects a cost-push external shock rather than demand pressures, leaving the medium-term disinflation trajectory broadly intact. As a result, the policy framework holds a cautious and data-dependent stance, balancing short-term inflation risks against still-fragile domestic demand conditions.

Externally, the oil shock dominates, while activity has been resilient. Oil prices have increased significantly, remaining above USD 90 per barrel in the weeks leading up to the IPoM’s statistical cutoff (June 10), driven by geopolitical tensions in the Middle East. This has led to a generalized increase in inflation across economies. At the same time, global activity remains resilient, supported in part by technological investment and relatively favorable financial conditions, and also boosting the copper price scenario. This combination of stronger external demand and higher imported inflation creates a layer of uncertainty over the speed at which domestic inflation can converge to target.

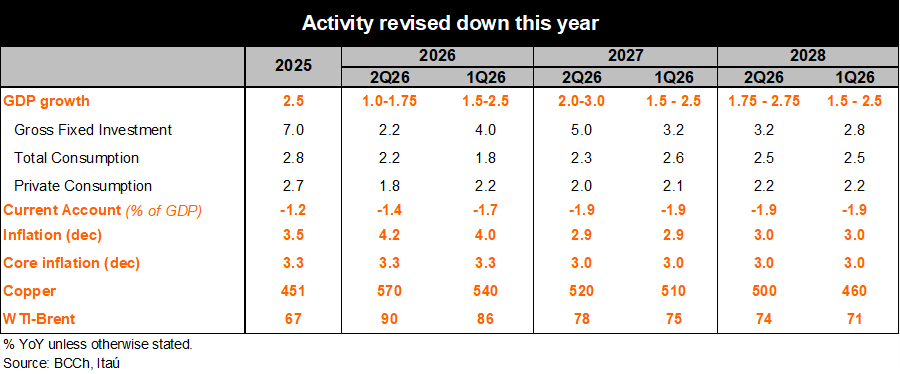

Short-term growth downgraded, yet improved in the medium-term. The BCCh revised down its 2026 growth forecast (from 1.5%-2.5% to a 1.0%-1.75% range), primarily reflecting a weaker-than-expected first quarter driven by declines in mining, agriculture, and other resource-based sectors. These sectors have exerted a disproportionate drag on activity, with additional spillovers into construction and selected services. Importantly, the limited propagation of these shocks implies only modest effects on the output gap, reducing the urgency for a policy response. Labor market conditions have softened, with higher unemployment, weak job creation, and a shift toward informality. At the same time, rising inflation has eroded real wage growth and weighed on consumer sentiment. As a result, private consumption is expected to play a smaller role in driving growth, particularly in the near term. However, the medium-term outlook improved, with higher projected growth in 2027 (revised from 1.5%-2.5% to 2.0%-3.0%) supported by a more favorable investment trajectory. While investment (Gross Fixed Capital Formation) was revised down for 2026, particularly in machinery and equipment, the BCCh now expects a stronger recovery over the policy horizon. This is complemented by a larger-than-anticipated fiscal impulse, with public spending assumptions for 2026 revised up by 1.2pp of GDP relative to the March IPoM, partially offsetting weaker private demand.

Higher near-term inflation path but anchored medium-term outlook. Inflation has increased more rapidly than previously anticipated, rising to 3.9% year-on-year in May from 2.4% in February, largely due to higher fuel prices linked to the surge in global oil prices. This has pushed volatile inflation components higher, while core inflation has remained broadly stable and in line with prior projections, indicating that second-round effects remain contained thus far. Despite the short-term surge, the BCCh maintained its baseline scenario in which inflation converges back to the 3% target by around the second quarter of 2027. This reflects the assessment that the current shock is transitory and externally driven, with pass-through dynamics behaving in line with historical norms. Nevertheless, the higher short-term inflation path introduces greater uncertainty around the pace of convergence, particularly if cost pressures persist or broaden. The IPoM’s implicit CPI forecast for June is -0.15% MoM, and -0.07% MoM for core CPI.

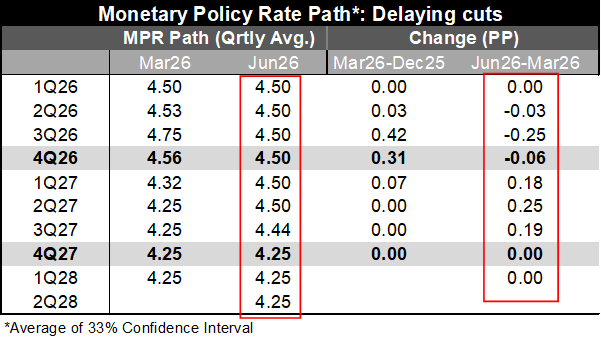

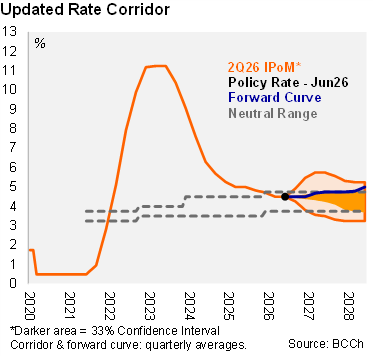

Monetary policy path signals slower, more conditional easing ahead. The mix between weaker activity and higher inflation leads the BCCH to adopt a cautious and flexible monetary policy stance. While the signaling remains of one 25bp cut to 4.25%, the center of the nominal neutral range, the path points to only starting during the latter part of 2027 (as opposed to early next year). Future decisions will be evaluated on a meeting-by-meeting basis, reflecting heightened uncertainty and the evolving balance of risks. Crucially, the nature of the growth slowdown—being largely supply-driven—reduces the need for aggressive monetary stimulus, while the temporary rise in inflation argues against a rapid pace of rate cuts. The scenario sees more balanced inflation risks, but uncertainty remains elevated. Upside risks could stem from the possibility of a more persistent oil price shock, stronger global growth, or larger fiscal impulse, all of which could delay the disinflation process, and justify higher rates. Meanwhile, prolonged weakness in key domestic sectors, particularly mining, as well as further deterioration in labor markets and consumption, along with a faster-than-expected normalization in energy prices could accelerate the return of inflation to target and bring forward the anticipated timing of lower rates.

Our Take: The June IPoM update comes broadly in line with expectations, highlighting a macroeconomic environment in which short-term shocks complicate, but do not fundamentally alter the medium-term outlook. The coexistence of weaker growth and higher inflation exacerbates the policy trade-off, leading the Central Bank to delay the timing of lower rates. With the latest developments in the Middle East and lack of significant second-round inflation pressures to-date, we expect the rate curve to consolidate around stable rates for the remainder of the year. We see broadly symmetric balance of risks going forward, resulting in limited conviction over the direction the next rate move.