2026/05/18 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

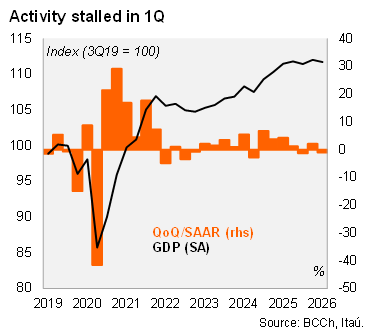

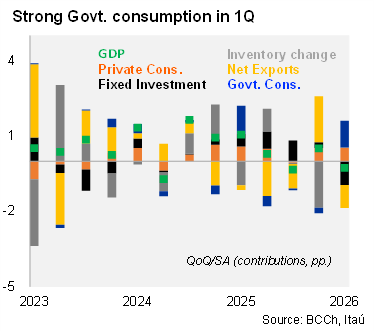

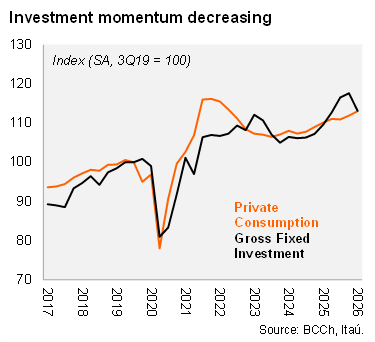

According to the Central Bank, 1Q26 GDP fell by 0.5% YoY, below market expectations and the preliminary Imacec reading of -0.3%. By expenditure components, private consumption rose 2.5% YoY (+2.8% in 4Q25), mainly driven by strong services consumption (health, transports, and restaurants & hotels). To a lesser extent, both spending on durable and non-durable goods also contributed positively. Government consumption grew 3% as a result of increased spending on health. Gross fixed capital formation increased 3.2% YoY (+9.7% in 4Q25), with machinery and equipment expanding 10.1% (+23% in 4Q25; in line with still positive capital imports) while construction declined 0.9% (+1.3% in 4Q25). However, weaker GDP print was mainly explained by the result of net exports. Exports of goods and services fell 4.9%, because of lower shipments of fruits and copper (total agro exports recorded a -23% YoY, while copper exports decreased 6.8%). On the other hand, total imports rose 2%, where imports of goods increased 1.7% due to higher imports of electrical and electronic equipment, transportation equipment, and crude oil. Our April Imacec Nowcast points to 0.8% YoY contraction.

Activity dynamics stalled at the margin. Activity contracted 0.3% QoQ (+0.5% in 4Q25; 1Q recorded the same number of working days as the previous year, with zero calendar effect for the period). Non‑mining GDP receded 0.1% in 1Q26 (+0.5% in 4Q). On the expenditure side, private consumption increased 1% QoQ/SA, with all components contributing positively, while government consumption recorded a sharp 7.2% (-1.4% in 4Q). Gross fixed capital formation decreased 3.8%, with both of its components recording negative prints, and reversing the strong momentum seen in previous quarters (+0.9% in 4Q). Finally, GDP contracted 1.1% QoQ SAAR in 1Q, after rising 2.1% in 4Q.

Our take: These figures reinforce the signs of short-term weakness in economic activity. Our estimates place the statistical carry-over for this year at a modest 0.03%, suggesting limited inherent growth momentum. Against this backdrop, our 2.1% annual growth forecast faces meaningful downside risks, particularly as tighter global financial conditions and higher oil prices are likely to further weigh on activity. In this context, the overall softness in the economy also reduces the likelihood of rate hikes by the Central Bank of Chile in the near term, especially considering the improvement in inflation expectations.