2026/05/20 | Diego Ciongo & Soledad Castagna

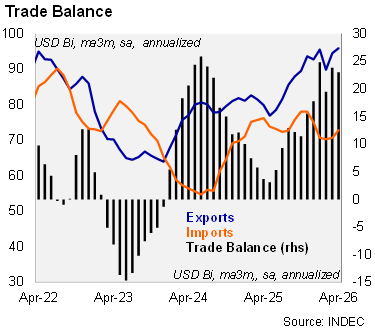

Argentina recorded a USD 2.7 billion trade surplus in April, a sharp improvement from the USD 0.2 billion surplus a year earlier and well above market expectations (USD 1.8 billion, central bank survey). On a rolling basis, the 12‑month trade surplus widened to USD 18.3 billion, up from USD 15.8 billion in March. The seasonally adjusted annualized trade balance fell to USD 23.0 billion, from USD 23.8 billion in the previous month.

Export performance strengthened across all sectors. Total exports rose 21.2% yoy in the quarter ended in April, accelerating from 17.2% in 1Q26. Agricultural exports (including processed products) increased by 17.0% yoy, just below the 17.8% pace recorded in 1Q26. Exports of other industrial products surged 26.4% yoy, an acceleration from 23.7% in 1Q26. Sequential dynamics were also supportive, with exports rising 1.5% qoq (saar) in April.

Imports contracted but recover at the margin. Imports declined 4.7% yoy in the quarter ended in April, after falling 7.3% yoy in 1Q26. Capital goods and parts imports plunged 13.6% yoy, while consumer goods imports (including vehicles) rose 2.5% yoy. Intermediate goods imports rose by 3.6% yoy. On a sequential basis, imports expanded 12.8% qoq (saar) in April, reversing the 21.2% drop in the previous month, representing a good signal for the domestic demand at the margin.

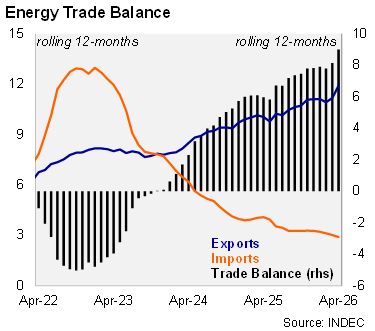

The energy trade balance continued to improve. The rolling 12‑month energy surplus reached USD 9.0 billion in April, up from USD 8.2 billion in the previous month and USD 7.8 billion in December 2025. Energy exports grew 28.8% yoy in the quarter ended in April, while oil imports declined sharply (42.3% yoy).

Our take: We revised our 2026 trade surplus forecast to USD 18 billion, from USD 14 billion in our previous scenario, reflecting stronger‑than‑expected readings in recent months. While exports should maintain solid momentum—supported by a favorable outlook for soybean and corn harvests, alongside firmer oil prices—the ongoing recovery in imports is set to partially offset these gains. Having said that, a larger‑than‑expected trade surplus should allow the central bank to scale up its FX purchases, which have already reached USD 8.5 billion year‑to‑date. May trade data is due on June 18.