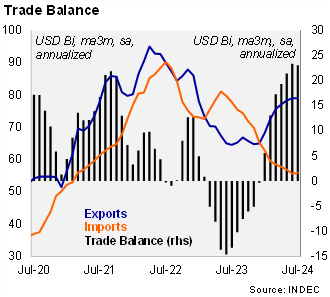

The trade balance rose to a surplus of USD 1.6 billion in July, well above the USD 0.7 billion deficit registered in the same month of 2023. The surplus was slightly below market expectations according to the central bank's survey, with analysts estimating a surplus of USD 1.7 billion. The 12-month rolling trade balance rose to a surplus of USD 10.6 billion in July, from USD 8.3 billion in the previous month. At the margin, the seasonally-adjusted annualized trade balance fell slightly to a surplus of USD 23.0 billion in July, from a surplus of USD 23.3 billion in the previous month.

Exports increased in the quarter ended in July, driven by the normalization of the agricultural sector, after last year’s severe drought. Total exports rose by 21.0% yoy in the quarter ended in July, after a 18.2% gain in 2Q24. Agricultural exports, including manufactured agricultural products, expanded by 24.3% yoy in the period (up from 22.0% yoy in 2Q24). Exports of other industrial products rose by 7.1% yoy in the same period, up from an increase of 1.3% yoy in 2Q24. On a sequential basis, exports rose by 10.2% qoq/saar in July.

Imports fell again, amid a weaker currency and soft activity. Total imports fell by 28.3% yoy in the quarter ended in July (from a drop of 30.5% yoy in 2Q24), down by 11.8% qoq/saar in the period. Imports of intermediate goods fell by 27.3% yoy in the period, and imports of capital goods decreased by 28.7% yoy, while imports of consumer goods (including cars) decreased 14.9% yoy.

Energy trade surplus also increased in July. The rolling 12-month balance reached USD 4.1 billion in July, from a surplus of USD 3.6 billion in the previous month and only USD 0.1 billion in 2023. Energy imports plummeted by 37.4% yoy in the quarter ended in July, while oil exports rose by 41.0% yoy in the same period.

Our Take. We project a trade surplus of USD 15 billion for 2024, representing a significant turnaround from the USD 6.9 billion deficit recorded in 2023. The rapid improvement of external imbalances reflects the effectiveness of the macro stabilization program.