2026/04/09 | Diego Ciongo & Soledad Castagna

Manufacturing activity contracted on a sequential basis in February.

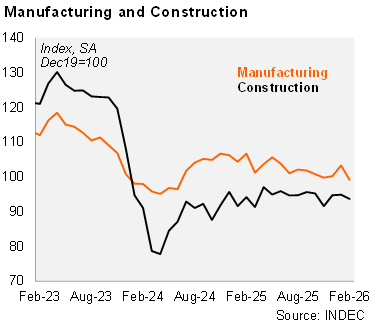

The manufacturing component of the IPI declined by 4.0% MoM/SA in February, reversing the 3.1% MoM/SA increase recorded in January. Despite this setback, industrial output edged up 0.1% QoQ/SA in the quarter ended February. On an annual basis, manufacturing output fell 8.7% YoY in February and 5.3% YoY in the quarter ending that month. Sectoral performance remained weak, with only one out of nine subsectors posting year‑on‑year growth in February.

Construction activity also softened sequentially. The construction index declined 1.3% MoM/SA in February, after a modest 0.2% MoM/SA increase in January. However, construction output posted a 0.3% QoQ/SA expansion in the quarter ended in February. In annual terms, construction fell 0.7% YoY in February but expanded by 0.9% YoY in the moving quarter. Employment in the sector increased 3.6% relative to January 2025 (with a one‑month lag), suggesting some underlying resilience in labor demand. Survey data point to broadly stable expectations. Among private construction firms, 69.3% expect activity to remain unchanged over the next three months, while 17.8% anticipate an increase and 12.9% foresee a decline. Expectations among public‑works‑oriented firms are slightly more cautious: 16.8% expect a decline, 63.2% foresee no change, and 20.0% anticipate greater activity.

Our take: We forecast 2026 GDP growth of 3.5%, supported by an improving investment outlook and a favorable statistical carryover. However, the persistent acceleration in inflation represents a key downside risk, potentially delaying the recovery in real wages and warranting a more cautious view on the pace of the consumption rebound. In addition, leading investment indicators, including imports of capital goods, have yet to signal a near‑term recovery, suggesting that the investment upturn may materialize more gradually than initially expected.