2026/03/20 | Diego Ciongo & Soledad Castagna

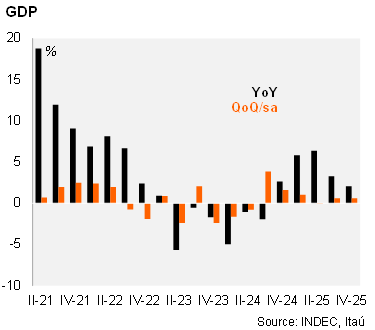

GDP increased by 0.6% qoq/sa in 4Q25, matching the pace recorded in the previous quarter. This outcome came in below the 0.8% qoq/sa suggested by the monthly activity proxy (EMAE). On an annual basis, GDP expanded 2.1% YoY in 4Q25, slowing from 3.3% YoY in 3Q25. As a result, GDP grew by 4.4% in 2025, marking the second consecutive year of positive annual growth. The statistical carryover into 2026 stands at 0.7% (0.8% according to the EMAE).

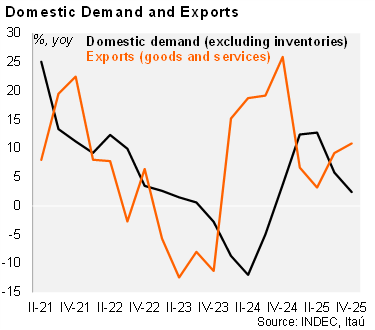

Final domestic demand—driven primarily by private consumption and investment—rose 0.6% qoq/sa in 4Q25, rebounding from a 0.7% decline in the previous quarter. Private consumption increased by a solid 1.7% qoq/sa, while gross fixed investment contracted by 2.8% qoq/sa. Public consumption also declined, falling 1.0% qoq/sa over the quarter.

On an annual basis, domestic demand (excluding inventories) expanded by 2.4% YoY, reflecting a robust 4.1% YoY increase in private consumption. In contrast, gross fixed investment declined by 2.1% YoY, while public consumption edged down by 0.1% YoY. On the external front, exports rose by 10.9% YoY, broadly matched by a 10.1% YoY increase in imports.

Our take: We forecast GDP growth of 3.5% in 2026, underpinned by a firmer outlook for investment and private consumption, alongside a favorable statistical carryover. That said, the recent acceleration in inflation tempers our optimism regarding a real wage recovery, warranting a more cautious stance on the pace of the consumption rebound. Separately, leading indicators for investment such as imports of capital goods have yet to signal a recovery in the near term.