2026/03/16 | Diego Ciongo & Soledad Castagna

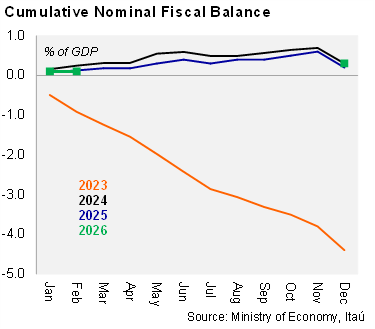

Argentina recorded another fiscal surplus in February. The primary surplus reached 0.4% of GDP in the first two months of the year, while the nominal fiscal surplus, including debt interest payments, was 0.1% of GDP. These figures were like those from same period of 2025.

Soft real tax revenues. Total real revenues fell by 5.5% YoY in the quarter ended in February after a 6.4% decline in 4Q25. Tax collection dropped by 7.8% YoY in real terms during the period, following a 7.3% decrease in 4Q25. The weak performance in tax collection was still affected by a drop in export duties due to their temporary suspension in 4Q25, along with a decline in VAT and income tax, which is likely due to soft consumption.

Primary expenditures declined in February. Primary expenditures fell by 2.3% YoY in real terms during the quarter ended in February, following a 3.9% YoY decrease in 4Q25. Payrolls decreased by 11.0% YoY (-12.3% in 4Q25) affected by higher inflation at the margin, while transfers to provinces fell by 4.7% YoY (-21.4% in 4Q25). Furthermore, capital expenditure decreased by 1.3% YoY, after falling 2.4% in 4Q25. On the other hand, energy subsidies rose by 40.5% YoY in real terms, compared with a drop of 5.3% in 4Q25, while pension payouts rose by 3.4% YoY in real terms (+6.1% in 4Q25) also affected by higher inflation at the margin.

Our Take: Our 2026 primary surplus forecast stands at 1.5% of GDP, in line with the official forecast presented in the 2026 Budget. This forecast is supported by disciplined fiscal management.