2026/02/24 | Diego Ciongo & Soledad Castagna

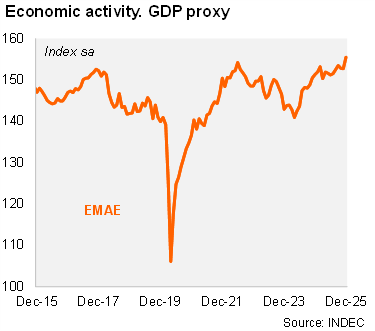

Activity rose sequentially in 4Q25, marking the second consecutive quarterly gain. According to the EMAE (official monthly GDP proxy), economic activity expanded by 1.8% MoM/SA in December, following a contraction of 0.1% MoM/SA growth in November. Thus, activity expanded by 0.8% QoQ/SA in December, after growing 0.6% QoQ/SA in September. On an annual basis, activity rose by 3.5% in December and expanded by 2.2% in 4Q25 (3.3% yoy in 3Q25). Thus, the statistical carryover for 2026 stood at 0.8%.

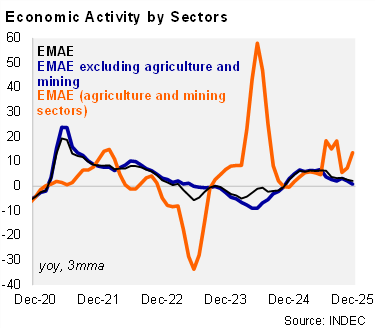

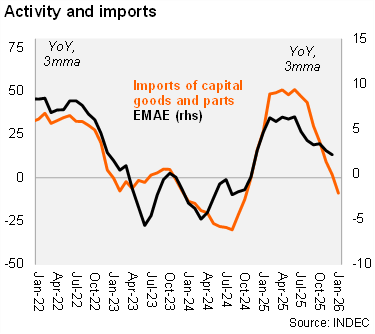

All sectors expanded on an annual basis in 4Q25, except manufacturing. Primary activities rose by 13.6% YoY during this period (compared to +18.4% YoY in 3Q25), while services (including the commerce sector) expanded by 1.4% YoY (vs. 2.1% in 3Q25). Moreover, construction rose by 1.1% YoY (from -0.4% YoY in 3Q25). On the other hand, manufacturing fell by 4.8% YoY (vs. a drop of 4.6% YoY in 3Q25), in line with lower capital goods and parts imports.

Our take: For 2026, we expect a slowdown to 3.5%, partly due to a lower carryover. A better outlook for investment and private consumption aided by lower interest rates should drive growth during the year, despite an apparently weak start. However, we are more skeptical about the recovery of real wages given higher than expected inflation at the start of the year. The national accounts data for 4Q25 will be published on 20 March, while the January 2026 EMAE figures will be published on 26 March.