2026/05/21 | Diego Ciongo & Soledad Castagna

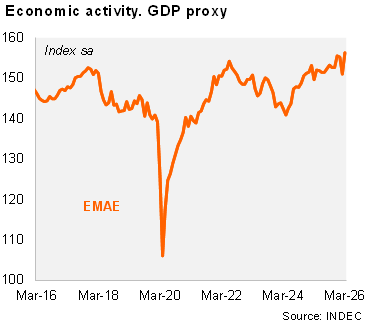

Economic activity expanded sharply on a monthly sequential basis in March. The EMAE (monthly GDP proxy) rose 3.5% MoM/SA, after falling 2.7% MoM/SA in February and 0.2% MoM/SA in January. As a result, activity expanded by 0.4% QoQ/SA in 1Q26, decelerating from 0.8% in 4Q25. On an annual basis, output rose 5.5% YoY in March and 1.7% in 1Q26, down from 2.0% YoY in 4Q25. The statistical carryover for 2026 now stands at 1.3%.

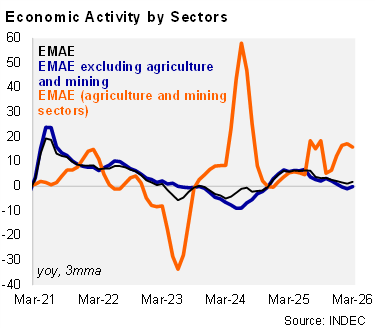

Most sectors expanded in 1Q26, with the exception of manufacturing. Primary activities surged 15.8% YoY, supported by a record agricultural harvest. Construction grew 2.1% YoY, accelerating from 0.9% YoY in 4Q25.

Services—including commerce—posted a modest 0.7% YoY expansion, down from 1.4% YoY in 4Q25, reflecting subdued domestic demand. By contrast, manufacturing contracted 2.3% YoY, in line with still-weak imports of capital goods and intermediate inputs.

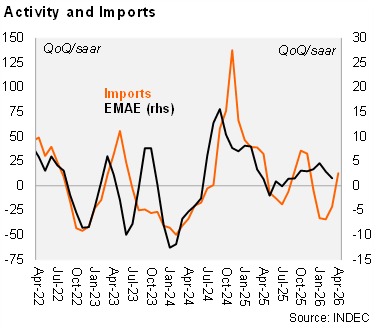

Our take: We maintain our 2026 GDP growth forecast at 3.5%, with risks tilted to the downside given a weak carryover from 1Q26. High-frequency indicators point to mixed momentum in April–May. External demand remained resilient, with exports and imports rising 1.0% and 0.8% MoM/SA in April, respectively. By contrast, domestic demand softened. Consumer confidence fell sharply in April (-5.7% MoM) and only partially rebounded in May (+1.3% MoM). Activity indicators also signal weakness on the consumption side, with retail sales declining 1.3% MoM/SA in April, reflecting still-constrained labor income and purchasing power. That said, ongoing disinflation coupled with lower interest rates should gradually support a recovery in real incomes, providing some upside to private consumption in the near term. The April EMAE release (June 29) will be key to gauge the strength of the early 2Q recovery.