2026/06/29 | Diego Ciongo & Soledad Castagna

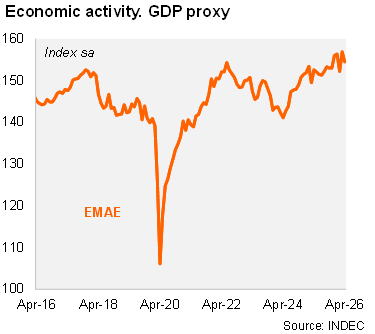

Economic activity contracted on a sequential basis in April. The EMAE (monthly GDP proxy) fell 1.5% MoM/SA, following a 3.1% increase in March. As a result, activity declined 0.4% QoQ/SA in the rolling quarter ending in April, down from +0.8% in 1Q26.

On an annual basis, output rose 1.6% YoY in April, while growth in the quarter ending that month reached 2.2% YoY, broadly stable compared to 2.3% in 1Q26. The statistical carryover for 2026 now stands at 1.4%.

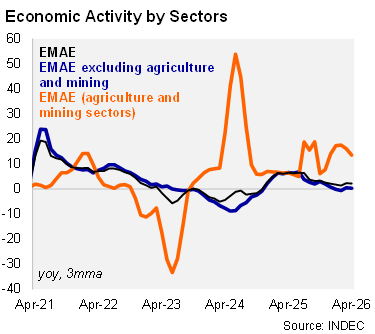

Most sectors expanded in the quarter ending in April, with the exception of manufacturing. Primary activities rose 13.0% YoY (down from +18.6% YoY in 1Q26), supported by a strong agricultural harvest. Construction increased 2.1% YoY, easing from 2.5% YoY in 1Q26. Services (including commerce) grew 0.7% YoY, down from 1.1% YoY in 1Q26, reflecting still-subdued domestic demand. In contrast, manufacturing contracted 1.9% YoY, consistent with weak imports of capital goods and intermediate inputs.

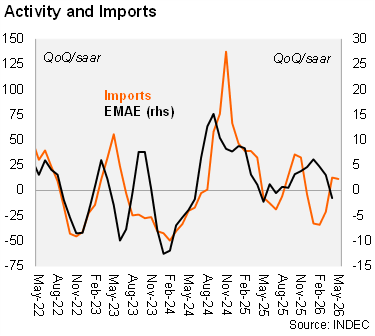

Our take: We maintain our 2026 GDP growth forecast at 3.5%, supported mainly by primary sectors, particularly agriculture, energy, and mining. The ongoing disinflation process and lower interest rates should gradually support a recovery in real incomes and private consumption. However, the banking system's NPLs rose further in May, across households and firms, signaling a note of caution. Investment is expected to recover with a lag; however, continued weakness in capital goods imports suggests that the trough may not yet have been reached. In addition, the still-low statistical carryover at the start of the year introduces downside risks to near-term activity dynamics. The May EMAE release (July 22) will be key to assess whether activity is regaining momentum in 2Q26.