2025/09/03 | Diego Ciongo & Soledad Castagna

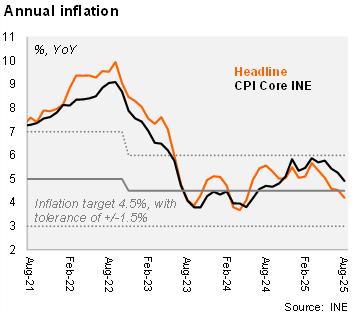

Inflation fell by 0.03% MoM in August (from +0.29 a year ago and a 5-year median of +0.54%), likely supported by a stronger UYU. The print was below our forecast and market expectations according to the BCU’s survey (0.2% MoM and 0.26% MoM, respectively). Notably, this is the fifth consecutive downside inflation surprise with respect to market consensus. The main monthly impact in August came from transport, which fell 0.72% MoM (incidence -0.08 p.p.), clothing which decreased 2.12% MoM (incidence -0.05 p.p.) and food and non-alcoholic beverages prices, which fell by 0.16% MoM (incidence -0.04 p.p.) due to lower vegetables and legumes prices (-3.90% MoM) and meat (-0.20% MoM). On the other hand, recreation, sports and culture rose by 0.54% MoM (incidence 0.03 p.p.), while education services increased by 0.71% (incidence 0.03 p.p.). Core inflation (excluding fruits & vegetables and fuel prices) increased by 0.07% MoM, from 0.39% MoM in August 2024. On an annual basis, headline inflation fell to 4.2% in August (from 4.53% in July), while core decreased to 4.92% from 5.25% in the previous month. We note that both readings remain within the Central Bank's tolerance range for its inflation target of 4.5% ± 1.5%. Moreover, headline inflation is now lower than BCU’s target.

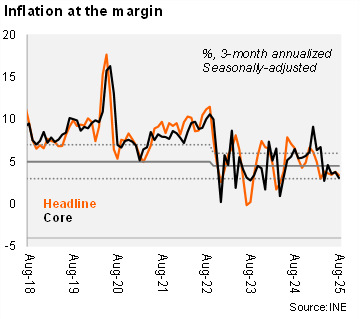

At the margin, headline and core inflation decelerated in August. Using our own seasonally adjusted figures, the three-month annualized headline inflation fell to 3.4% in August (down from 3.8% in July), while core inflation was 3.1% (down from 3.8% in the previous month).

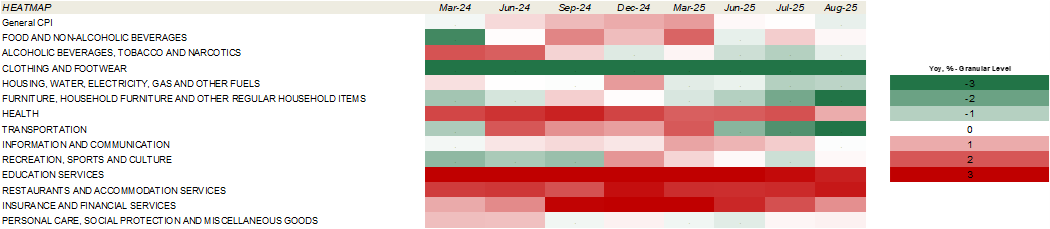

Our CPI heatmap shows that 46% of selected items are below the central bank’s target (4.5%), the same figure as the previous month (46%), but better than December 2024 figures (15%).

Our take: Due to lower-than-expected inflation figures and a stronger UYU, we see significant downside risks to our 4.5% inflation estimation for YE25. September's CPI will be released on October 3, and the next monetary policy meeting is scheduled for October 7. Given well-behaved inflation and falling inflation expectations, we anticipate that the BCU will reduce the policy rate by an additional 25 basis points to 8.50% at the next meeting.