2026/02/04 | Diego Ciongo & Soledad Castagna

Inflation rose by 0.92% MoM in January (from +1.1% a year ago and a 5-year median of 1.50%), below market expectations according to the BCU’s survey (+1.09% MoM), but in line with our call. The main monthly impact came from housing, electricity and water which rose by 2.45% MoM (incidence of 0.32 p.p.), given the reversal of the temporary energy discount in December, coupled with higher water and electricity tariffs. On the other hand, food and non-alcoholic beverages prices rose by 0.96% MoM (incidence 0.25 p.p.) due to higher vegetable fruits and meat prices. Transport prices dropped by 0.86% MoM (incidence of -0.09 p.p.) given lower fuel and flight tickets, amid a stronger UYU.

Core inflation (CPI CE VFC) (excluding fruits & vegetables and fuel prices) increased 0.91% MoM, from 0.98% MoM in January 2025. The CPI-CE VFCTA, which excludes almost 26% of the general basket (fruits and vegetables, fuels, and centrally priced or administered products) rose by 0.38% MoM, from 0.80% MoM in the same month one year ago.

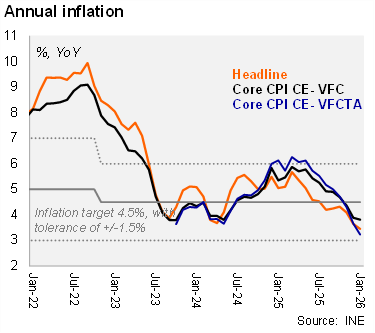

On an annual basis, all CPI readings drifted towards the floor of the target’s tolerance range. Headline inflation fell to 3.46% YoY in January from 3.65% in December, while the core reading decreased to 3.82% from 3.89% in the previous month. The CPI-CE VFCTA fell to 3.23% YoY, from 3.66% YoY in December.

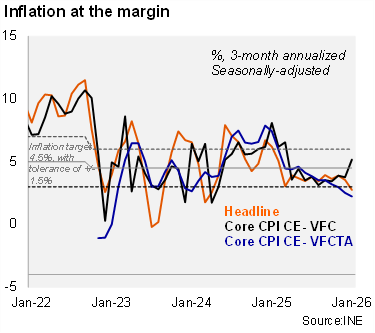

At the margin, headline and core inflation were mixed. Using our seasonally adjusted figures, the three-month annualized headline inflation fell to 2.8% in January (from 3.6% in December), while core inflation rose to 5.2% from 3.8% before. Finally, the CPI-CE VFCTA reading fell to 2.2%, from 2.5% in the previous month.

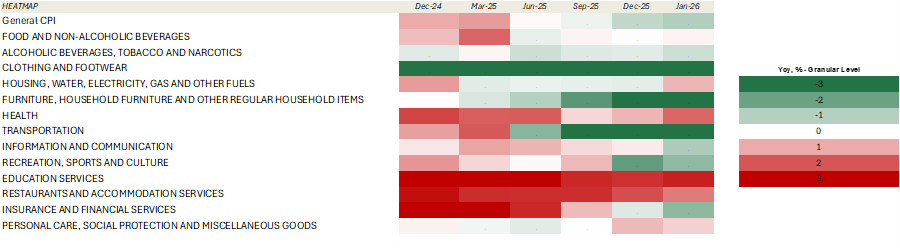

Our CPI heatmap shows that 54% of selected items are below the central bank’s target (4.5%), below the previous month (62%), and much better than January 2025 figures (38%).

Our Take: Our inflation forecast for YE26 stands at 4.5%, in line with the central bank's target, implying a rebound later in the year. January’s downside surprise relative to consensus takes place as inflation expectations have gradually edged lower towards the BCU’s target. February’s CPI will be released on March 4.