2025/10/01 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

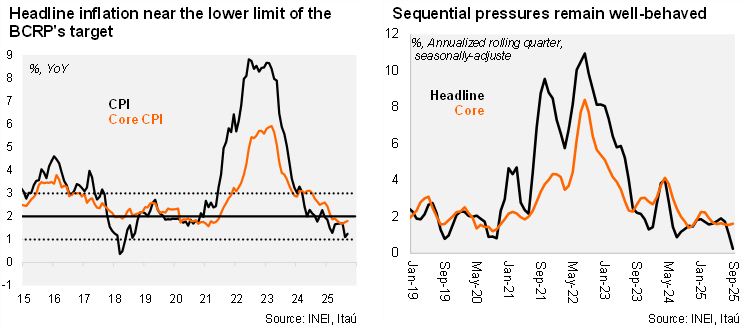

Consumer prices ticked up by 0.01% from August to September, below both the Bloomberg consensus and our call of +0.1% m/m. This marks the second consecutive downside surprise. The modest increase was primarily explained by higher prices in Restaurants and Hotels (+0.1% m/m), Miscellaneous Goods and Services (+0.13%), and Recreation and Culture (+0.15% m/m), which were offset by a decline in Food and Non-Alcoholic Beverages (-0.1% m/m). Core inflation, which excludes volatile food and energy components, rose by 0.06% m/m.

Sequential price pressures are low. On a year-over-year basis, headline inflation increased from 1.1% in August to 1.25% in September, marking ten consecutive months with inflation in the lower half of the target range (1%-3%). Sequentially, headline inflation reached only 0.2% QoQ/SAAR. Core inflation edged up slightly to 1.8% y/y (from 1.75% y/y in August) and sequentially sits at a similar rate of 1.6% QoQ/SAAR. Importantly, survey-based one-year inflation expectations have remained anchored within the target range since December 2023, reaching 2.2% in August.

Our take: We expect headline inflation to rise moderately in the coming months, partly due to base effects, reaching 2% by year-end. The balance of risks remains tilted to the downside, particularly if favorable exchange rate dynamics and lower oil prices persist. Given the benign inflation outlook, we anticipate an additional 25 bp rate cut this year, bringing the policy rate to 4%. With the output gap largely closed and the policy stance only slightly restrictive, there is limited urgency to continue easing at next week’s meeting. The October inflation print will be released on November 1, and we preliminarily forecast a 0.1% m/m increase.