2025/09/26 | Diego Ciongo & Soledad Castagna

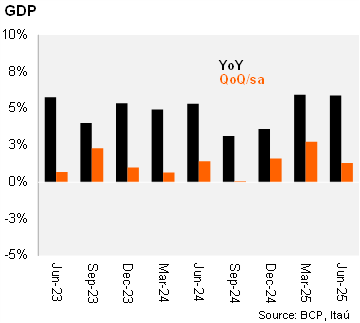

GDP expanded by 5.9% YoY in 2Q25, maintaining the annual pace from 1Q25. Looking at the breakdown on the supply side, the annual print was driven by the positive performances in services (+6.8% yoy) led by the commercial sector, manufacturing (+4.3% yoy), construction (+4.5% yoy) and the electricity sector (+14.3% yoy) due to greater water flow in the Paraná River. Conversely, the agricultural sector fell 3.1% yoy affected by a lower soybean harvest due to a moderate drought. At the margin, using our seasonally adjusted series, GDP rose sequentially in 2Q25 (1.3% qoq/sa), leaving the statistical carryover for 2025 at 5.4%.

Domestic demand improved in 2Q25. Internal demand increased by 12.4% year over year in 2Q25 (from 9.3% in 1Q25) driven by total consumption which expanded 3.0% yoy (from 4.4% in 1Q25). Private sector increased by 4.6% yoy, while the public sector declined by 5.9% yoy. Furthermore, gross fixed capital investment expanded by 22.4% yoy, led by the increases in investments in construction and in machinery and equipment. The external demand had a negative impact. Exports of goods and services rose by a mere 0.1% (from +0.3% in 1Q25), due to the positive results in exports of machinery and equipment as well as restaurant and hotel services ,likely helped by the spillovers from Argentina, offset by lower soybean sales. Moreover, the imports of goods and services expanded by 15.1% (from 9.0% in 1Q25) due to higher sales of machinery and equipment and chemical products.

Our take: We foresee significant upside risks to our 4.3% GDP growth forecast for this year given a high carryover. On the demand side, we expect private consumption to continue supporting growth.