2025/12/01 | Julia Passabom & Mariana Ramirez

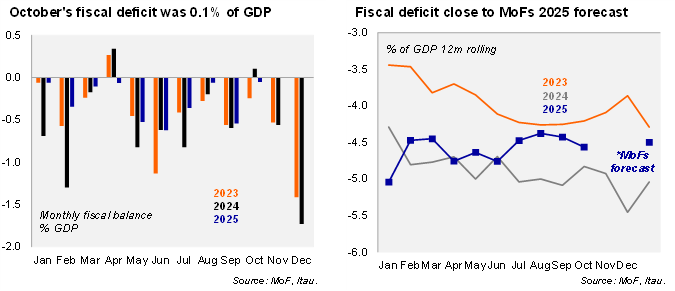

The Ministry of Finance (MoF) released its public finance report for October. On a 12-month rolling basis, the broadest measure of the public balance (PSBR) posted a deficit of 4.6% of GDP through October, while the primary public balance swung to a surplus of 0.6% of GDP. During the first ten months of the year, real revenues rose by 6.6% YoY, supported by greater-than-expected import taxes, VAT revenues, and oil revenues through the Mexican Oil Fund for Stabilization and Development and the income tax collected from new contracts and allocations in the field of hydrocarbons. On the other hand, total real expenditure increased by 1.7% YoY, primarily due to administrative branches and social programs, despite contractions in capital investment. Finally, net government debt stood at 51.1% of GDP, below the MoF’s 2025 forecast of 52.3%. The historical figures presented as a share of GDP were revised, incorporating the changes in the historical nominal GDP made by INEGI at the end of November.

Our view: October’s figures indicate that the pace of revenue improvement continues to slow, with budgetary revenues below the target at 85.0% for the first ten months of 2025. Expenditures reached 98.9% of the budget as of October and 82.7% of the total approved budget for 2025. For 2025, we anticipate fiscal consolidation with a nominal deficit of 4.3% of GDP, rising net government debt to 52.3%, and a primary surplus of 0.3%, in a context of lower interest payments compared to the previous year. However, when incorporating the revised figures for nominal GDP, the forecast deteriorates with higher deficit of 4.5%, government debt of 53.6% and a primary surplus of 0.2%. Looking forward, despite the measures included in the 2026 budget to increase revenues, such as the increased use of technology in customs and higher taxes on products from countries without a trade agreement with Mexico, we believe additional revenue-enhancing measures may be needed in the future. We also remain cautious regarding the sustainability of continued transfers to Pemex to meet its increasing market debt and bank loan obligations.

See more details below .