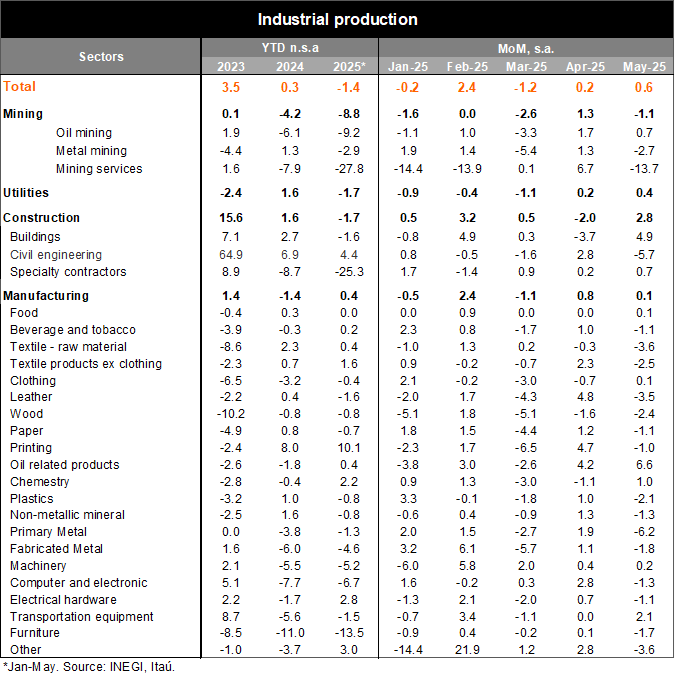

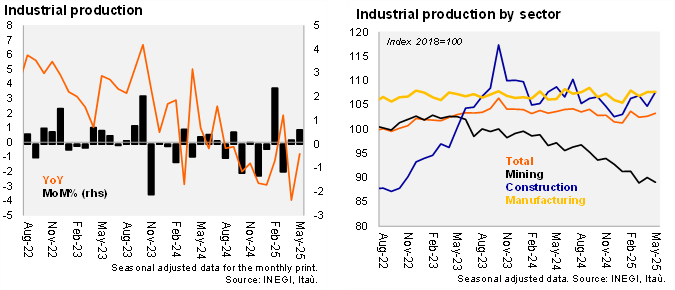

Industrial production (IP) decreased by 0.8% YoY in May, which was a positive surprise compared to Bloomberg’s market consensus and our forecast, both at -1.9%. A favorable calendar effect due to Holy Week and a slight revision for April’s figure led to a mixed sectoral behavior: construction remained unchanged, manufacturing increased by 0.5%, mining contracted by 8.4%, and utilities fell by 3.7%. Using seasonally adjusted figures, IP increased by 0.6% MoM, performing better than consensus at -0.1%, our forecast at 0.0%, and INEGI’s nowcast of +0.1%. This performance was driven by growth in construction (2.8%, with expansion in building construction and specially contractors), manufacturing (0.1% MoM, with 6 out of 21 subsectors increasing), and utilities (0.4%). Mining partially offset the increase, contracting by 1.1% due to oil and mining services. Momentum in the industrial sector improved in May, with the QoQ/SAAR at 2.5%.

Our take: Today's release showed a positive bias as of May, with the QoQ/SAAR at 2.5% due to manufacturing and construction, despite mining’s negative performance. Looking ahead, as we’ve mentioned in recent months, shifts in U.S. trade policy will generate distortions in manufacturing exports, such as temporary inventory accumulation and a reorganization of supply chains. Additionally, high uncertainty is likely to be reflected in low levels of private investment in Mexico, which should imply weak private construction and manufacturing going forward. The government is focused on strengthening domestic activity amid changes in the global outlook, which might modestly drive public construction in the second half of 2025. We forecast a 0.2% GDP growth in 2025.

See more details below