2025/08/11 | Julia Passabom & Mariana Ramirez

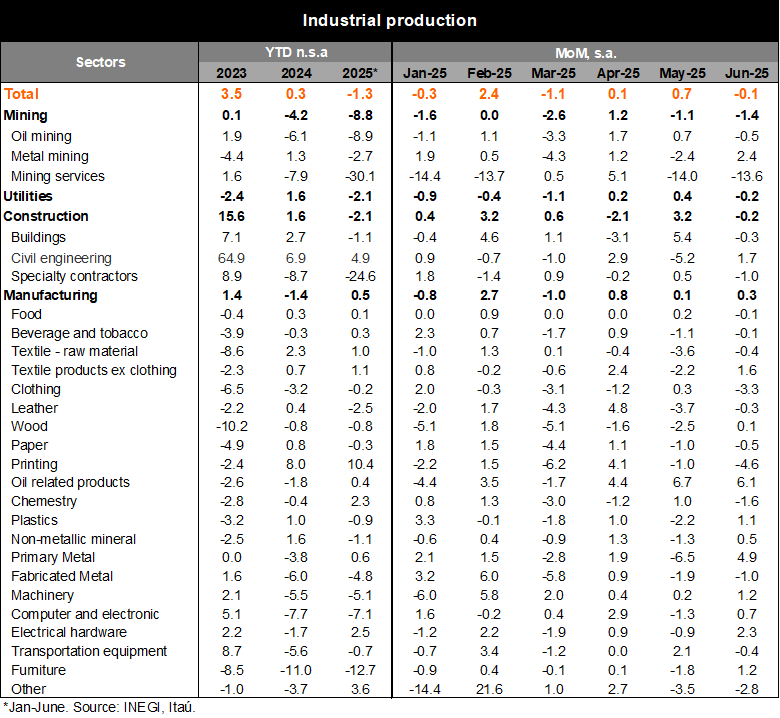

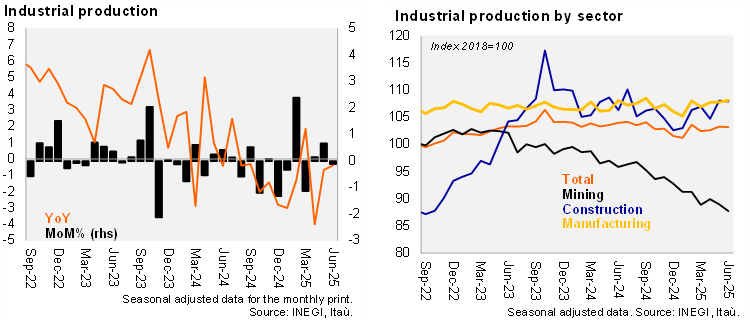

Industrial production (IP) decreased by 0.4% YoY in June, a negative surprise compared to Bloomberg’s market consensus of +0.2% yet closer to our forecast of -0.2%. The annual figures showed a contraction in mining of 8.6% and utilities of 3.7%, while manufacturing and construction increased by 0.7% and 1.7%, respectively. Using seasonally adjusted figures, IP decreased by 0.1% MoM, performing worse than consensus at +0.3%, our forecast at 0.0%, and INEGI’s nowcast of +0.2%. This performance was explained by a contraction in construction (-0.2%, with a decline in building construction), mining (-1.4% MoM due to oil and mining services), and utilities (-0.2%). Manufacturing partially offset the decrease, growing by 0.3%, with ten out of 21 subsectors increasing.

Our take: Today's release showed that the positive bias in activity continued through June, with the QoQ/SAAR at 2.3% due to manufacturing (4.4%) and construction (5.6%), despite mining’s negative performance (-7.1%). Looking ahead, as we’ve mentioned in recent months, shifts in U.S. trade policy will generate distortions in manufacturing exports, such as temporary inventory accumulation and a reorganization of supply chains. Additionally, high uncertainty is likely to be reflected in low levels of private investment in Mexico, which should imply weak private construction and manufacturing going forward. The government is focused on strengthening domestic activity amid changes in the global outlook, which might modestly drive public construction in the second half of 2025, with projects such as railways and highways. We forecast a 0.2% GDP growth in 2025, with a positive bias.

See more details below