2025/08/07 | Julia Passabom & Mariana Ramirez

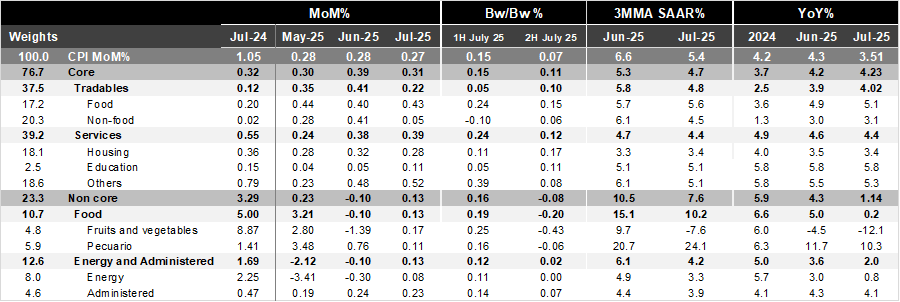

Bi-weekly headline CPI for the second half of July was 0.07%, below Bloomberg’s market consensus of 0.10% and our forecast of 0.19%. Core inflation came in at 0.11%, also below both the market's expectations of 0.12% and our forecast of 0.15%. Within the core component, tradable prices rose by 0.10% 2w/2w, up from the previous fortnight's 0.05% due to inflation in non-food merchandise. Services prices increased by 0.12% 2w/2w, down from the previous data of 0.24% due to less pressure in other services. The non-core component decreased by 0.08% 2w/2w due to deflation in agricultural prices, which fell by 0.20% during the fortnight in items such as chicken, avocados, and tomatoes.

In annual terms, headline inflation decelerated to 3.51% in July from 4.32% in June, remaining below the 4% threshold since the second half of April. Core CPI was relatively stable, moving slightly from 4.24% in June to 4.23% now, with tradables at 4.02% (up from 3.91%) and services at 4.44% (down from 4.62%). In the June 26 monetary policy statement, Banxico forecasted headline inflation at 4.3% and core inflation at 4.1% for 2Q25, slightly above the current headline rate of 4.08% and below the core rate of 4.18% for the same period. Core measures remain under pressure, despite some marginal relief: core CPI is at 4.7% 3MMA SAAR, with tradables at 4.8% and services at 4.4%. Within services, the pressure eased in other service categories.

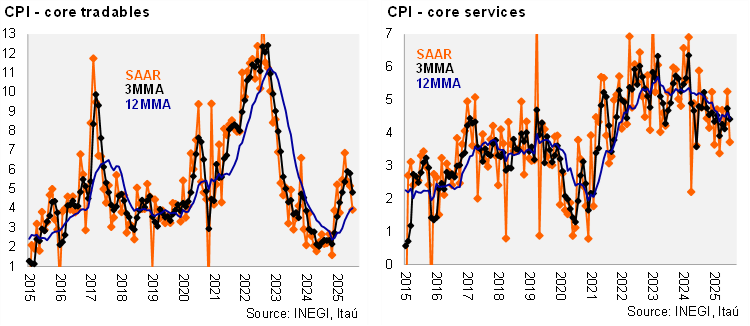

Our take: Today’s report reinforces our view that the disinflation process has already occurred, with headline inflation projected to oscillate around the ceiling of Banxico’s inflation target tolerance range, down from nearly 9% at its peak in 2022. Goods inflation remains high at the margin, although it appears to be peaking, and the current USDMXN appreciation should support additional disinflation ahead. Services inflation is decelerating, albeit at a slower pace, which aligns with labor market dynamics and sticky prices in this sector. We forecast CPI to end 2025 at 4.1% and 3.7% in 2026. Regarding the policy rate, we maintain our call for a 25-bps rate cut at today’s meeting, bringing it down to 7.75%. Banxico may cut further, conditional on inflation dynamics and the Fed. We expect only one 25-bp cut by the Fed this year, in December.

See details below