2025/10/09 | Julia Passabom & Mariana Ramirez

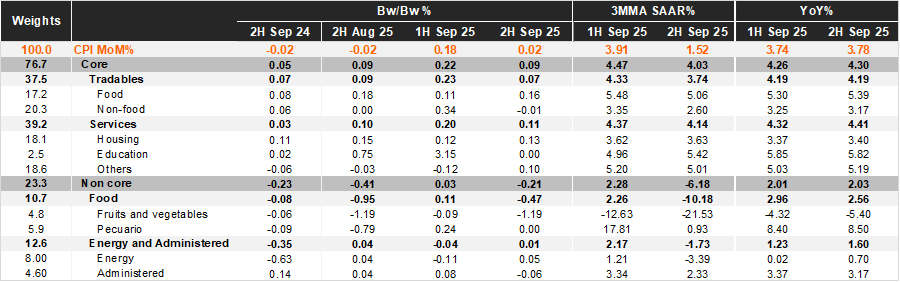

Bi-weekly headline CPI for the second half of September rose by 0.02%, below Bloomberg’s market consensus and our forecast, both at 0.08%. Core inflation came in at 0.09%, in line with our forecast but slightly below the market's expectations of 0.10%. Within the core component, tradable prices rose by 0.07% 2w/2w, down from the previous fortnight's 0.23%, due to food merchandise prices, despite deflation in non-food prices. Services inflation increased by 0.11% 2w/2w, down from the previous data of 0.20%, driven by housing and other services. The non-core component decreased by 0.21% 2w/2w due to deflation in the agricultural and tariffs components, which fell by 1.19% and 0.06% during the fortnight, respectively.

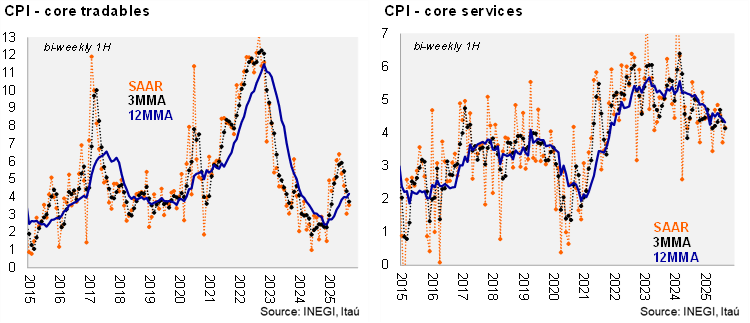

In annual terms, headline inflation rose to 3.76% in September, remaining below the 4% threshold since the second half of April, mainly supported by non-core inflation. Core CPI was relatively stable, moving slightly to 4.28%, with tradables at 4.19% (up from 4.05%) and services at 4.36% (down from 4.40%). We continued to observe significant marginal relief in core inflation: core CPI is at 3.9% 3MMA SAAR, with tradables at 3.6% and services at 4.0%. Within services, the pressure came from education due to the 2025-2026 school year, which represents a shift from the traditional August start.

Our take: Today’s report continues to show improvements in core inflation dynamics, which remain above 4% year-over-year in September, but is now considerably better at the margin. We forecast the CPI to end 2025 at 4.1% and 2026 at 3.7%. Regarding monetary policy, our current scenario anticipates another 25-bp cut in November to 7.25%. Barring any shocks, the current dynamics -strong USDMXN and an overall declining CPI trajectory- remain in place, and in the context of a widening negative output gap, Banxico is likely to maintain its forward guidance (plural) in November as well, pointing towards an extension of the cycle into 2026. We expect the monetary policy rate to be 7.0% in 2025 and 6.5% in 2026, with consecutive cuts.

See details below