2025/12/23 | Julia Passabom, Mariana Ramirez & Ignacio Martínez

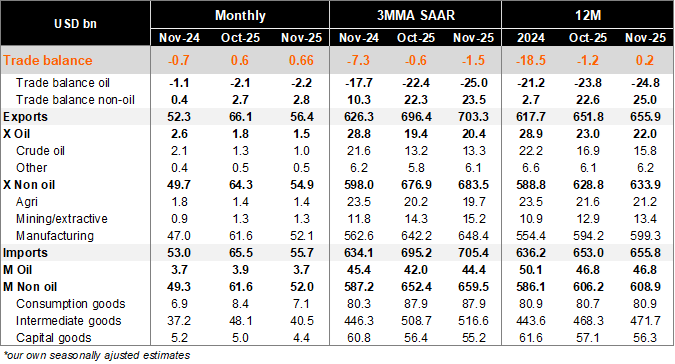

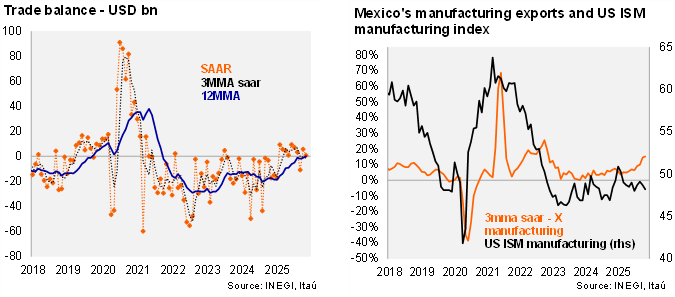

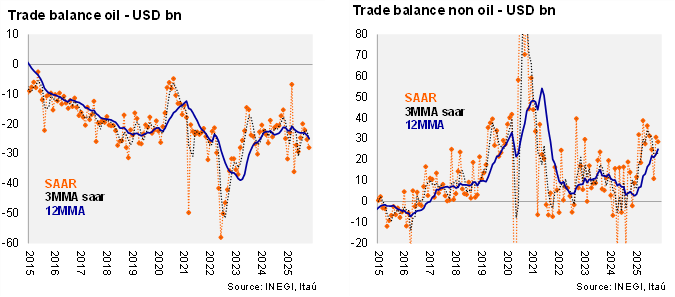

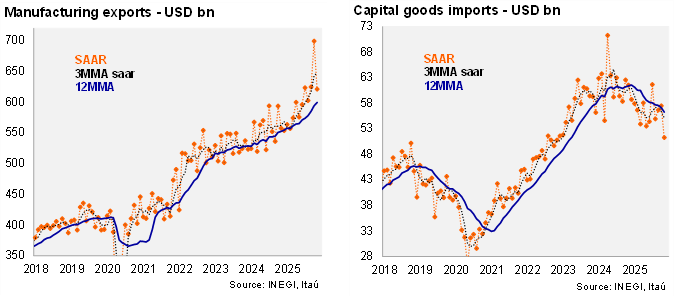

November’s trade balance revealed a goods surplus of USD 662.8 million, exceeding Bloomberg’s market consensus of a USD 451.5 mm deficit and improving upon November 2024’s deficit of USD 706.2 mm. On a 12-month rolling basis, the goods trade balance improved to a surplus of USD 189.9 mm, from a USD 1.2 bn deficit in October. However, at the margin, using three-month annualized seasonally adjusted figures, the trade balance showed some deterioration, now indicating a deficit of USD 1.5 bn (down from a USD 600 mm deficit in October). Worth mentioning that this is due a weak base effect from the September’s data. Examining the breakdown on a 12-month rolling basis, the oil trade balance continued to show a deficit (USD 24.8 bn deficit compared to a USD 25.0 bn surplus for non-oil), following the decline in domestic oil production and the government's strategy to prioritize domestic oil refineries. Manufacturing exports continue to be the highlight of the year, while capital goods imports are losing strength at the margin, leaving investments adjustments yet to materialize.

Our view: The better-than-expected trade balance in November follows a series of strong external data. Today’s release showed exports increasing at the margin, especially in the non-auto manufacturing sector, although there was some correction from the very strong numbers in October. Net exports are an important driver of economic growth in 4Q25, though less so than in 1Q25. Uncertainty surrounding Mexico’s trade relationship with the US will continue to challenge trade flows until a definitive USMCA renegotiation begins before July 1, 2026. Looking ahead, oil exports will be influenced by domestic policies related to national sovereignty and oil price dynamics, while manufacturing exports are expected to remain at high levels.

See detailed data below