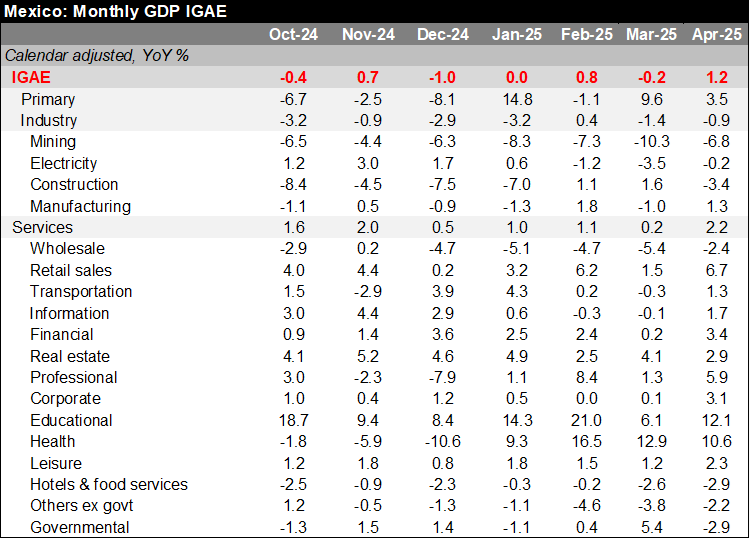

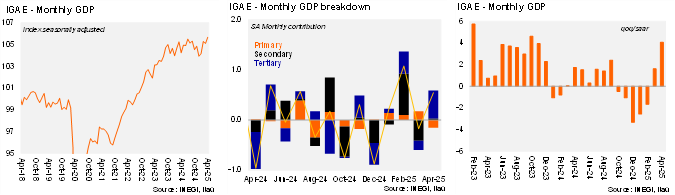

Economic activity decreased by 1.5%, a smaller contraction than Bloomberg’s market consensus and our forecast (-1.9% and -3.2%, respectively). INEGI revised March data downward, resulting in a slightly lower base effect for April. There was a positive calendar shift during the period, as the Holy Week vacation was in March in 2024, while this year it was in April. After adjusting for the calendar, the economy increased by 1.2%, driven by the positive performance of the services sector (+2.2%, with 10 out of 14 subsectors showing growth) and the agricultural sector (+3.5%, following solid growth in March). This growth occurred despite a contraction in industry (-0.9%, with declines in mining, electricity, and construction).

When considering seasonally adjusted figures, the economy rose by 0.5% MoM (IGAE nowcast at -0.3% MoM). In terms of sectors, industrial production increased by 0.1% MoM due to growth in mining, manufacturing, and electricity. Services increased by 0.9%, with positive performances in 10 out of 14 subsectors, including retail sales, transportation services, and financing services. Primary activities decreased by 3.7% MoM, following four months of increases.

Our view: Today's release showed a positive bias as of April, with the QoQ/SAAR at +4.1% with a positive broad-base performance across sectors. Looking ahead, we expect the economy to continue decelerate on an annual basis, with a few elements supporting its performance. For instance, the government is focused on strengthening domestic activity amid changes in the global outlook, which should become more evident in the second half of the year. Our 2025 GDP forecast was recently revised up to a modest 0.2% growth.

See details below